U.S. Credit Unions Adopt Tokenization of Real World Assets

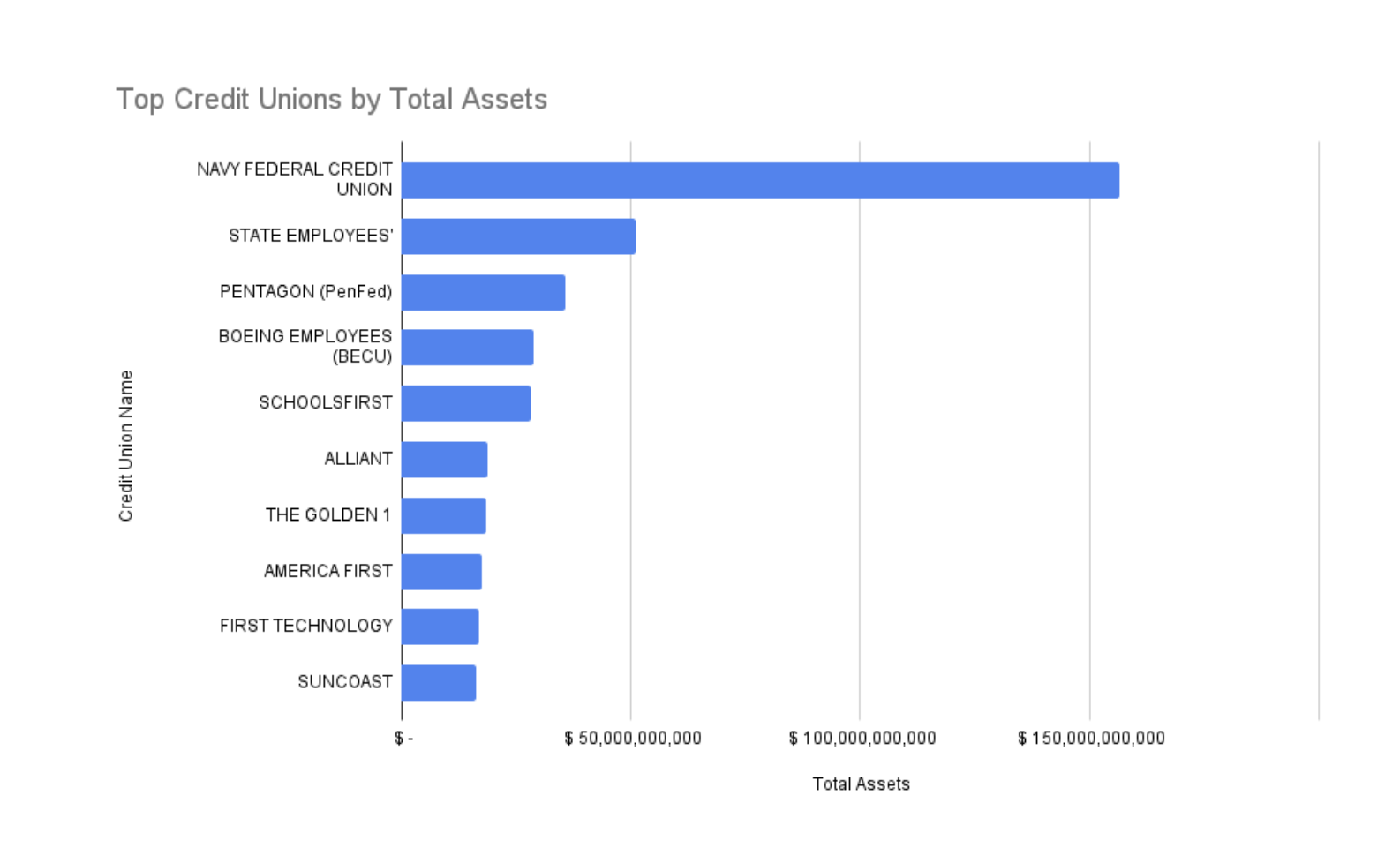

Traditional banks may still dominate the financial industry in terms of assets held, but credit unions are becoming an increasingly popular option for Americans who qualify. Recent data shows that there are roughly 4,600 credit unions in the United States. A September 2023 report from The National Credit Union Administration (NCUA)further notes that nearly 139 million Americans were members of federally insured credit unions, up 20% from five years prior.In addition, the credit union market size measured by revenue totaled $126.2 billion last year.

Credit Unions Are Ripe For Tokenization of Real World Assets

John Wingate, Chief Executive of financial platform BankSocial, told Cryptonews that a credit union is a member owned bank. “Unlike for profit banks that are owned by shareholders, credit unions are owned by the members, one member, one share, one vote,” said Wingate. “Given this, the credit union ethos and the decentralized fiance (DeFi) ethos are perfectly aligned.”While this may be true, credit unions face a number of challenges that may hamper future growth.

Kyle Hauptman, Vice Chairman of the NCUA – an independent U.S. government agency that regulates federal credit unions – told Cryptonews that credit unions buy and sell pieces of loans.

“This is a clunky process called ‘loan participations,” said Hauptman.

A compliance blog from the National Association of Federally Insured Credit Unions explained that loan participation occurs whenever the ownership interests in a loan are divided up and sold.

“Under section 701.22, federally insured credit unions (FICUs) can buy participation interests in loans under certain conditions,” the blog states.

Hauptman pointed out that the current loan participation process can be complex. For example, he explained that if a credit union makes a loan and another credit union buys a 20% stake in it, it gets 20% of every loan payment.

Hauptman noted that the credit union that buys participation in the loan doesn’t know if the payment has actually been made, however. Additionally, that credit union is unsure if the selling credit union will pay the required 20%.

“This makes it difficult for the buying credit union to plan, and it creates unnecessary uncertainty,” said Hauptman.

Tokenization Use Cases

Considering the challenge, Hauptman believes that tokenizing loans that aren’t big enough to be securitized in a bond offering may be helpful. “A smart contract would automatically pay the buying credit union their 20%,” said Hauptman. “That credit union will never have to ask ‘did they make a payment?’ or ‘when do I get my piece?.’”Ravi de Silva, Managing Partner at compliance risk management firm de Risk Partners, told Cryptonews that tokenization could also help manage compliance risk by providing greater transparency, security, and efficiency.For example, de Silva believes that tokenization would be helpful for credit unions and Anti-Money Laundering (AML) use cases.“Transaction monitoring is a key control requirement in AML, which involves analyzing customer transactional data to identify potential suspicious or fraudulent activities,” de Silva said. “Tokenization can enable efficient analysis of transactional data.”For instance, de Silva remarked that tokens can be used as a unique identifier to track transactional patterns and detect anomalies. He added that credit unions can analyze token data to detect large cash transactions, structuring or unusual transaction patterns. “AML regulations also require financial institutions, including credit unions, to perform thorough customer due diligence and maintain accurate records of their customers’ identities,” de Silva mentioned. Therefore, he believes tokenization can further help securely store and reference customer identification data.

Credit Unions Adopt Tokenization

Given the benefits that tokenization can bring to credit unions, it shouldn’t be surprising that some have started implementing these solutions. According to Wingate, BankSocial is working with several credit unions for use cases such as tokenizing identity.“Credit unions are using our ‘verified product’ for interoperable use between systems and fintechs, deposits for interoperability between bank accounts, other banks, and for DeFi use cases,” he said. Wingate explained that BankSocial’s verified product tokenizes transactional data through hashing. “This is done in a quantum resistant way, on-chain, to provide immutability to records and outcomes for regulators and third party audits,” he said. “We have future cases in the pipeline for merchant payments, treasury management, and lending/borrowing.”Wingate added that Great Lakes Credit Union recently implemented BankSocial’s Real Time Payment Solution. The solution uses Hedera Hashgraph’s distributed ledger technology (DLT) to tokenize payments and deposits for peer-to-peer transactions made on the Hedera network. He added that BankSocial uses the immutable ledger on Hedera as transaction resilience for traditional financial rails.

We’ve partnered with @CornerstoneCUR to Future Proof your Credit Union with BankSocial Exchange!

Combat deposit outflows from member’s crypto purchases with our co-branded, self-custody exchange experience – safe, secure, and designed for Credit Unions!

🔹 Quick signup in 45… pic.twitter.com/OzwF22hTAm

— BankSocial.io (@BANKSOCIALio) March 28, 2024

Marshall Hayner, Metallicus’s Chief Operating Officer, told Cryptonews that Metallicus is also working with credit unions on blockchain solutions.

“Metallicus has built the Metal blockchain, which is a layer-zero blockchain to enable banks, credit unions, financial institutions, and fintechs to create interoperable ledgers that can communicate seamlessly,” said Hayner.

A recent Forbes article noted that Metallicus is working with three credit unions, Vibrant, Meritrust Credit Union, and Fairwinds, to enable blockchain-based solutions.

Credit Unions Embrace Tokenization, But Concerns Remain

While it’s notable that some credit unions have begun exploring tokenization use cases, regulatory concerns are a constant challenge.According to Hauptman, the big question that credit unions face is whether or not tokens are securities. “Credit unions worry if that participation may be deemed a security,” he said. “We at NCUA have cleared the way for tokenization use, but we can’t really assuage other concerns about the tokens themselves.”Hauptman added that KYC processes, along with which platforms custody tokens, is a concern for credit unions.“And then within the platform the concern is ‘who are the node operators?’” Hauptman pointed out. “There’s already been political questions about a node being in North Korea or Iran. No one needs an OFAC investigation for breaking sanctions.”On a positive note, Hauptman shared that credit unions are moving forward with blockchain projects that enable identification.“This is where any token is clearly not something ever ‘bought or sold,’” he said. “But tokenization for real world assets remains an issue.”Yet, all things considered, Hauptman believes that U.S. credit unions are still better off implementing tokenization use cases than U.S. banks. He believes this is because NCUA has delivered guidance that provides positive clarity around regulations for credit unions. For example, Hauptman noted that in July 2021, NCUA published a “Request for Information and Comment on Digital Assets and Related Technologies” report. Later that year, NCUA released a report called “Guidance on Relationships with Third Parties that Provide Services Related to Digital Assets.” Additionally, in May 2022, NCUA released another document called “Guidance on Federally Insured Credit Union Use of Distributed Ledger Technologies.”

Credit Unions Should Work With Compliance Teams

In addition to clear guidance, de Silva believes that the regulatory challenges of implementing tokens can be solved by demonstrating how tokenization is implemented, monitored, and audited. “Credit unions need to continuously monitor their tokenization processes and conduct regular risk assessments to identify and address any vulnerabilities or emerging threats,” he said. “This includes staying updated on the evolving regulatory landscape and making necessary adjustments to ensure compliance.”Given this, de Silva pointed out that credit unions should work closely with compliance teams to adopt industry best practices for tokenization. “It is essential to establish a robust framework that aligns tokenization practices with applicable regulations, while prioritizing the security and privacy of customer data,” he said.

- CLARITY Act Senate Vote Locked In, But 60-Vote Hurdle Looms Large

- Mark Zuckerberg Meta AI Predicts an XRP Surge Few Saw Coming

- Microsoft Copilot AI Predicts the Price of XRP by The End of 2026

- Google Gemini AI Predicts the Price of Bitcoin by The End of 2026

- XRP Price Is Stuck Grinding Near Multi-Week Lows: What Happens at $1.05 Next?

2M+

250+

8

70

- CLARITY Act Senate Vote Locked In, But 60-Vote Hurdle Looms Large

- Mark Zuckerberg Meta AI Predicts an XRP Surge Few Saw Coming

- Microsoft Copilot AI Predicts the Price of XRP by The End of 2026

- Google Gemini AI Predicts the Price of Bitcoin by The End of 2026

- XRP Price Is Stuck Grinding Near Multi-Week Lows: What Happens at $1.05 Next?

More Articles