This Digital Asset Manager Has a Framework for Crypto Investing in 2020

2020 could be “one of the brightest years” that the digital asset industry has seen so far, finds Vision Hill,a New York-based full service digital asset management firm. They also provided a framework for how investors can think about approaching the digital asset market next year.

Their report explains that this opinion is not price-related, but that we’ll see the industry maturating faster. The company expects the public digital asset market to continue recovering next year, showing that there’s a need for a more diversified approach to the liquid and illiquid markets. Therefore, according to Vision Hill, 2020 will see:

- on the crypto-native side, more layer-1 mainnet launches and continued innovative breakthroughs across the technical spectrum,

- on the institutional side, a fast increase of the market sophistication, in terms of education, infrastructural advancements and product offerings.

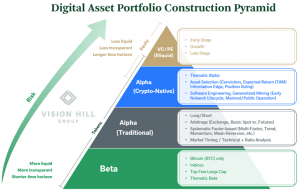

Actionable framework for digital asset portfolio construction in 2020

The company came up with four-category segmentation that they say provides a framework for how investors in 2020 can think about approaching the crypto market.

Beta (a measure of volatility, risk): 2020 will bring more growth in simple, passive, low-cost structures to capture beta; the spread of single asset vehicles is expected to increase; many vehicles will want to fill the gap left by the delayed approval of an official Bitcoin Exchange-Traded Fund (ETF) by the U.S. Securities and Exchange Commission (SEC); acquiring shares in an ETF is unlikely for 2020; and active managers will begin to specialize in differentiated sources of alpha generation that will complement beta position.

Alpha (a measure of the active return on an investment) will be coming from two distinct sources in this space:

a) traditional alpha strategies from traditional markets: there are many traditional market strategies that seem to transfer well into digital assets, and there will be more specialized strategies producing different sources of alpha generation; more liquidity will enter the market, and if liquidity expands, it will lead to diversified trading and faster development of new derivative markets for other assets; the trading fees will go down due to the global competition for liquidity;

b) unique sources of alpha that are crypto-specific in nature, as alpha generated by crypto-native strategies is unique to this asset class and requires specific, difficult-to-acquire expertise. Examples include:

- thematic alpha, coming from early identification of trends: already funds are focusing their entire investment mandate on a specific theme within digital assets (e.g. DeFi (decentralized finance), commodity monies, Web3, infrastructure, privacy), and some of the thematic verticals may become more apparent in 2020;

- asset selection: several assets have outperformed Bitcoin (BTC) on a year-to-year basis, and this will continue as market participants return to a risk-taking mentality, but also rotate out of large cap digital assets and into selective smaller cap ones;

- generalized mining strategies will see a continued growth, but will start looking differently; it can be segmented into different categories, with different kinds of firms specializing in different stages; smaller hedge funds are likely to focus on the early stages of lifecycles of their carefully selected networks, and larger funds are likely to focus on the later stages of network lifecycles (the mainnet/public operation);

- exchanges will continue to grow as the dominant centers of liquidity and will continue to leverage across all their service lines, becoming well-positioned to run large scale generalized mining operations and create secondary income streams as a byproduct of their business; they could commoditize validation revenue (especially commissions and transaction fees) by trending it down to zero and still remain profitable thanks to the revenue from other sources, the report says.

Traditional venture

This is related to illiquid venture capital and private equity investments that enable and support the development of the digital asset ecosystem, the report explains. The market will see more clarity next year as more token economic experiments get launched and more data gets collected and studied.

“While it remains to be seen whether it’s better to invest in tokens or in equity with respect to gaining blockchain exposure,” the report says, “we believe that equity-only investors are missing the transformative investment opportunity this asset class presents.”

2019 Takeaways

Finally, the report also highlights the firm’s top 10 takeaways of this year:

- the industry is segmented into two main categories: Bitcoin and everything else; BTC is currently the safest digital asset in the blockchain space, also attractive for its USD 120 billion network size;

- Bitcoin is maybe market beta currently; the combination of its size and institutionalization make it an attractive first step for allocators to get exposure to the digital asset market – a trend which will accelerate;

- substantial progress was made on growing institutional investor interest, but a small amount of institutional capital has made it into the space (c. USD 200 billion);

- there was a shift away from complexity and toward simplicity, e.g. the growth of bitcoin-focused products or simpler fund structures;

- every active manager tracked by the company has relatively underperformed passively holding Bitcoin; its parabolic ascents challenge the ability of active managers to outperform BTC during the windows they occur;

- the majority of blockchain application activity has occurred on Ethereum, with DeFi becoming a primary area of focus;

- there was a move away from crypto as money/payment and a means of exchange, and toward digital assets for financial applications and economic utility;

- there was a continued proliferation of supply side services across various networks, but very little demand side activity to meet them;

- while Ethereum leads the space on adoption, smart contract competitors have launched their chains, with a noticeable accelerative pace of innovation (technologically, economically and socially);

- crypto is likely to have a trickle and flood effect in many forms and through many interactions by all different kinds of people, driven by convenient quality products offering solutions, already seen happening in 2019.

__

Learn more:

11 ‘Bold’ Crypto Predictions for 2020 by Blockchain Capital

Read Messari CEO Ryan Selkis’ 19 Bitcoin, Ethereum Forecasts for 2020

Check our Crypto 2020 series for more predictions:

- Google’s Gemini AI Predicts Incredible XRP Price For Next 90 Days

- Elon Musk Grok AI Predicts Explosive Bitcoin Price by The End of 2026

- Bitcoin Price Prediction: Andrew Tate Liquidated for 108 Times, Now He Doubles Down With 40x BTC Long

- XRP Price Is Targeting $1,000 Says Ex Goldman Analyst

- Crypto News, June 17: Kevin Warsh First FOMC, Binance vs. MiCA as CZ Takes on Hyperliquid, and BTC USD Grinds Sideways

2M+

250+

8

70

- Google’s Gemini AI Predicts Incredible XRP Price For Next 90 Days

- Elon Musk Grok AI Predicts Explosive Bitcoin Price by The End of 2026

- Bitcoin Price Prediction: Andrew Tate Liquidated for 108 Times, Now He Doubles Down With 40x BTC Long

- XRP Price Is Targeting $1,000 Says Ex Goldman Analyst

- Crypto News, June 17: Kevin Warsh First FOMC, Binance vs. MiCA as CZ Takes on Hyperliquid, and BTC USD Grinds Sideways

More Articles