SEC Faces Criticism from Commissioners Over FlyFish NFT Case

The U.S. Securities and Exchange Commission (SEC) has initiated a heated debate following its enforcement action against Flyfish Club, LLC, for the unregistered sale of non-fungible tokens (NFTs) used as memberships to an exclusive dining experience.

The SEC’s decision revolves around the argument that Flyfish’s sale of NFTs, used to grant access to a luxury restaurant, violated securities laws because buyers could potentially earn profits through resale or leasing.

However, dissenting commissioners Hester Peirce and Mark T. Uyeda argued that these NFTs are utility tokens designed for access rather than investment, emphasizing that the SEC’s overreach could stifle innovation in the NFT space.

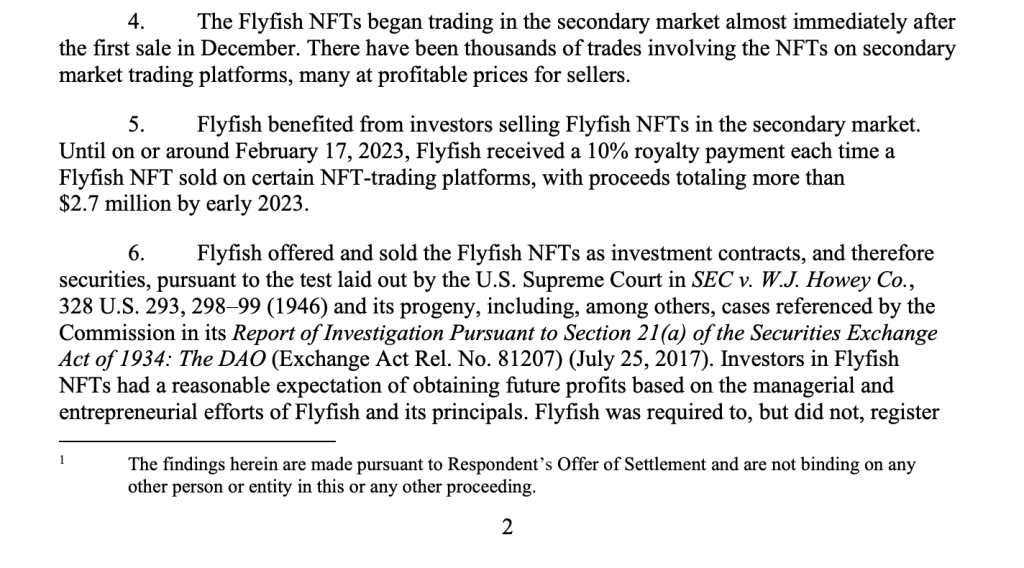

SEC Action Against Flyfish Club: Are NFTs Now Securities?

The SEC charged Flyfish Club for raising approximately $14.8 million by selling 1,600 NFTs between August 2021 and May 2022.

The NFTs functioned as memberships to an upcoming high-end dining club in New York, granting holders exclusive dining privileges upon the restaurant’s opening.

The sale garnered widespread attention, not only due to its unique integration of NFTs into a traditional membership model but also because of its resale potential.

According to the SEC, this resale potential and Flyfish’s public statements about building a large business model with future clubs and events positioned the NFTs as security offerings under U.S. law.

The regulatory agency argued that Flyfish violated Sections 5(a) and 5(c) of the Securities Act of 1933 by failing to register these NFTs as securities before offering them to the public.

Flyfish’s structure allowed for profit-making opportunities, such as earning passive income through leasing the NFTs, which the SEC cited as evidence that the NFTs met the criteria outlined by the Howey Test.

As a result, the SEC imposed a $750,000 civil penalty on Flyfish Club and ordered the company to cease selling its NFTs and destroy any remaining tokens within ten days.

Commissioners Peirce and Uyeda’s Dissent

Despite the SEC’s firm stance, commissioners Hester Peirce and Mark T. Uyeda issued a rare public dissent, openly criticizing the agency’s actions in this case.

In their joint statement, the commissioners argued that the Flyfish NFTs were clearly utility tokens intended to provide a tangible benefit—access to an exclusive dining experience—rather than serve as speculative investment vehicles.

“You need it to eat at the Flyfish Club,” they wrote, explaining that the token’s utility was for membership access, not for speculative gains.

While acknowledging that some buyers might have purchased the NFTs with the intent of resale or leasing, the commissioners emphasized that this possibility should not automatically classify the tokens as securities under the Howey Test.

They stressed that the NFTs had a “concrete use” and that the potential for resale profit was incidental rather than central to the NFT’s purpose.

Peirce and Uyeda also expressed concerns over the SEC’s intervention in this case, warning that such regulatory actions could stifle innovation in the rapidly evolving NFT space.

They argued that by treating utility NFTs as securities, the SEC imposed an unnecessary regulatory burden on creators and businesses, limiting their ability to experiment with new technologies and business models.

The commissioners criticized the SEC’s broad application of securities laws to NFTs, particularly those that offer access to unique experiences, like Flyfish’s dining memberships.

“Securities law is not needed everywhere,” they argued.

They suggest that clearer guidelines should be provided for businesses operating in the NFT space to ensure they can innovate without fear of violating securities regulations.

- Elon Musk Grok AI Predicts XRP Will Do This by Next 30 Days, and Nobody Is Ready

- Ethics Provision Deal Could Unlock Senate Vote on the Clarity Act

- XRP Price Prediction: Can Korean Demand Trigger XRP’s Next Breakout?

- Senate Ethics Deadlock Drags CLARITY Act Odds Under 40% on Polymarket

- XRP Price Could Turn Volatile This Month: What’s at Stake for Ripple?

2M+

250+

8

70

- Elon Musk Grok AI Predicts XRP Will Do This by Next 30 Days, and Nobody Is Ready

- Ethics Provision Deal Could Unlock Senate Vote on the Clarity Act

- XRP Price Prediction: Can Korean Demand Trigger XRP’s Next Breakout?

- Senate Ethics Deadlock Drags CLARITY Act Odds Under 40% on Polymarket

- XRP Price Could Turn Volatile This Month: What’s at Stake for Ripple?

More Articles