What is an NFT and How Does It Work?

An NFT, or non-fungible token, is a unique digital asset, like art or music, stored on a blockchain. This blockchain technology ensures that each NFT is unique and can be easily identified and impossible to duplicate. These characteristics give it its value digitally.

To be “non-fungible” means that these tokens are one-of-a-kind and not interchangeable, unlike cryptocurrencies like Bitcoin or Ethereum, which are fungible and can be exchanged for one another.

NFTs attach a digital certificate of ownership to the file, secured through blockchain technology. This digital certificate allows the NFT’s owner to verify its authenticity. When a transaction using an NFT is done, it will be recorded on the blockchain, and the ownership certificate will be transferred to the buyer. In contrast, the original file remains accessible to others online.

Key takeaways

- An NFT, or non-fungible token, is a unique digital asset on the blockchain with a secure digital ownership certificate that ensures authenticity and non-interchangeability.

- To create an NFT, you must mint it to record it on the blockchain, which ensures its uniqueness, ownership, and security via smart contracts.

- NFTs now extend beyond art to include gaming assets, virtual real estate, memberships, and digital identities, though experts debate their long-term investment potential versus speculative risks.

Non-Fungible Token Meaning

When a token is described as non-fungible, it means that it is unique and irreplaceable. It also means that it cannot be traded on a one-to-one basis since each has distinct properties or characteristics. NFTs are unique on the blockchain, representing ownership of an exclusive digital item that cannot be swapped directly for another NFT, as each holds its specific value.

Cryptocurrencies, such as Bitcoin and Ethereum, are fungible assets, meaning that they are interchangeable. Each unit has the same value and can be exchanged equally with another. For instance, one Bitcoin is always equal to another Bitcoin, and one U.S. dollar is equal to another U.S. dollar. NFTs, on the other hand, don’t work like this since each token is individually identified, creating unique ownership.

To make these concepts easier to grasp, imagine this example: a bag containing one million dollars is a fungible asset since it can be exchanged for any other bag with the same value. In contrast, a work of art is unique and non-fungible because its specific characteristics and history make it distinct and valuable to different buyers.

What Is NFT Art?

NFT art is pieces of digital artwork that are configured as non-fungible tokens in a blockchain. This technology has changed the art industry because artists can now create exclusively digital pieces while being able to authenticate and sell their original digital works safely through tokenization.

This process of tokenizing digital artworks means that the asset owner uploads the piece to an NFT marketplace, where it is “minted” on the blockchain—recording it as a unique, unchangeable asset. After that, the artwork will be available to be sold to collectors, who will receive a blockchain-based proof of ownership, even though the digital file can still be viewed online. One successful example of an artwork traded as an NFT was the artist Beeple’s $69 million sale of his NFT artwork “Everydays: The First 5000 Days” at a Christie’s auction in 2021.

Some of the most reliable NFT marketplaces are OpenSea, Foundation, and SuperRare, which connect artists and collectors globally. These platforms opened the doors to the NFT market, providing artists with new revenue opportunities and enabling collectors to trade unique digital artworks with verifiable ownership, establishing NFTs as a major force in the digital art landscape.

How Do NFTs Work?

To create an NFT, the asset needs to go through the minting process. This process consists of recording the NFT on the blockchain, securing its uniqueness. When a creator wants to mint an NFT, it will upload the asset to an NFT platform, where it will be tokenized, meaning it’s given a unique identifier on the blockchain and becomes an NFT with distinct ownership.

Smart contracts are an important part of minting since they automate creating, selling, and transferring ownership of NFTs. These contracts contain code that dictates the terms of the asset, like ownership rights, resale royalties, and terms of sale. By verifying ownership directly on the blockchain, smart contracts allow buyers to confirm the NFT’s authenticity and its creator’s rights, securing the value and credibility of each asset.

Blockchain technology provides transparency, security, and proof of ownership in the minting process. Every NFT minted is recorded on a distributed ledger, meaning it can be tracked and verified publicly. Different blockchains support NFTs, each with unique attributes; Ethereum is the most widely used and offers robust security, while Solana provides faster transaction speeds at lower fees. Other networks, like Polygon and Flow, support NFT minting, expanding options for creators and collectors across various ecosystems.

What Is the Point of Having an NFT?

You might want to invest in NFTs for several reasons, including ownership, digital bragging rights, investment opportunities, and the desire to collect unique items. These assets allow investors to acquire the verified digital copy, giving them social status among collectors, especially for exclusive or highly sought-after pieces. Many investors also see NFTs as an investment, with hopes that the value of their assets will appreciate over time.

For artists, NFTs allow them to earn royalties and make direct sales without intermediaries, such as art galleries or buyers. Smart contracts on the blockchain can be programmed to pay creators a percentage every time their NFT is resold, creating a continuous revenue stream. This contrasts with traditional art and collectibles markets, where secondary sales rarely benefit the original creator. NFTs give artists more control over their work and direct access to their audience.

Additionally, by tokenizing their work as NFTs, artists can control the number of copies, creating rarity and increasing the demand. This concept of digital scarcity mimics the appeal of limited-edition items in traditional collecting, adding value to the asset and offering collectors a sense of exclusivity.

How NFTs Make Money

If you are planning to use NFTs to make money, here are the three main ways:

- Primary sales: This means you will buy the assets directly from the artist or in a marketplace during an initial sale. This strategy aims at the possibility that the asset’s price will increase; for example, NBA Top Shot launched digital collectible moments from NBA games as NFTs, which sold out quickly, generating millions in initial sales and creating a loyal fan base for future releases.

- Secondary sales: In this case, you will buy an asset that has already been sold, probably at a higher price. Projects like the Bored Ape Yacht Club have seen substantial price appreciation in the secondary market, with some apes initially bought for a few hundred dollars and later reselling for hundreds of thousands due to the community and exclusivity associated with ownership.

- Royalties for creators: When setting up smart contracts on their NFTs, creators can receive automatic royalty payments each time they are resold, ensuring ongoing earnings.

Whether you’re an investor or artist, these are the best NFT wallets to store your assets securely.

Types of NFTs and Use Cases

NFTs have multiple applications that can be summarized into these four categories:

NFT Art

This category includes pieces of artwork that underwent tokenization. This type of NFT allows creators to sell unique or limited editions of paintings, songs, photography, or any kind of digital work, with the blockchain serving as proof of authenticity. Notable examples include Paris Hilton’s “Planet Paris,” a series of short videos that helped Hilton earn millions of dollars.

Collectibles

Digital collectibles can also be a form of NFT, being a highly popular form of fandom and memorabilia. For instance, NBA Top Shot offers fans digital moments from basketball games, giving fans the chance to own, trade, and even profit from memorable sports moments.

In-game Assets

If you are playing blockchain-based games, you can buy elements such as virtual land, skins, and characters in the shape of NFTs. For example, in Decentraland, users purchase virtual real estate as NFTs to develop and interact within the digital world.

Real-world Assets

NFTs are also used to tokenize real-world assets, including real estate, deeds, and intellectual property. Through tokenization, ownership of tangible assets can be transferred more quickly and is secured by the blockchain. Real estate tokens on platforms like RealT enable fractional ownership and easier transfer of property rights.

NFT Marketplaces — Where and How to Buy and Sell NFTs

If you want to buy or sell NFTs, you must understand and explore some of the leading platforms offering this service. Here, we will overview some of them and give you step-by-step instructions on how to make money using NFTs.

- OpenSea: OpenSea is the largest and one of the most accessible NFT marketplaces. It supports a wide range of NFT types, from art and collectibles to domain names and virtual worlds. Its broad selection and user-friendly interface make it popular with beginners and experienced collectors alike.

- Rarible: Known for its community-driven approach, Rarible allows users to create, buy, and sell NFTs with added governance features. Rarible’s native token, RARI, gives users a say in platform decisions, fostering a decentralized and community-centric marketplace. For more information, read our complete Rarible review.

- SuperRare: SuperRare is a curated NFT marketplace specializing in high-quality digital art. Each piece on SuperRare is carefully selected, providing a gallery-like experience for users interested in exclusive, premium NFT art.

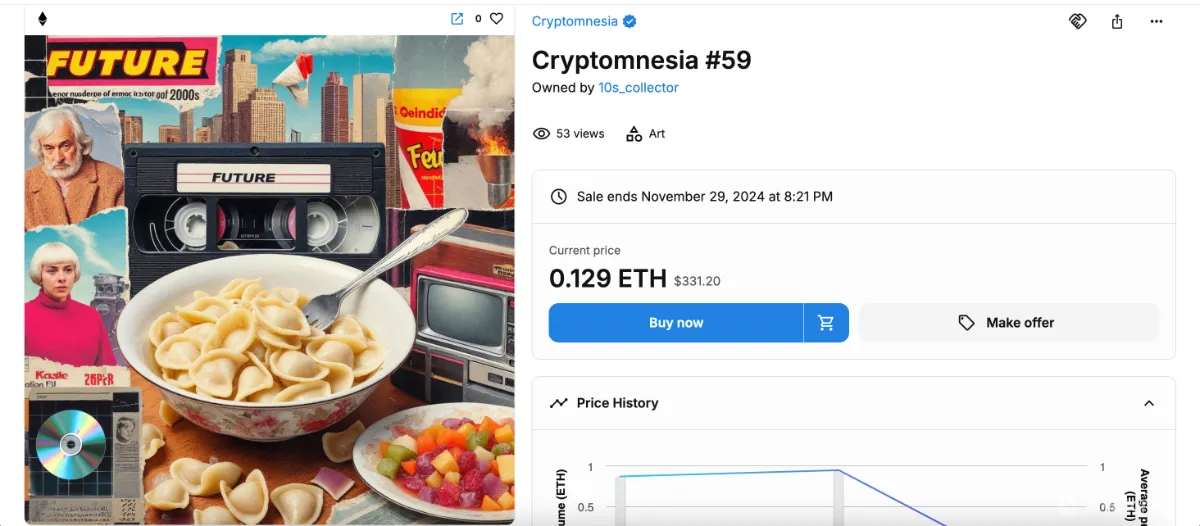

Buying NFTs in OpenSea

Here’s a quick guide to buying NFTs on OpenSea, one of the most popular marketplaces for digital collectibles.

- Go to the official OpenSea website and connect or create a wallet by clicking the icon in the upper left corner.

- Browse the website and find the asset you want to acquire.

- After finding the artwork you want to buy, click on it and select “Buy Now.” You can also make an offer at a different price, which the seller will either approve or deny within the indicated time.

- Confirm transaction details, including gas fees, and approve the purchase through your wallet.

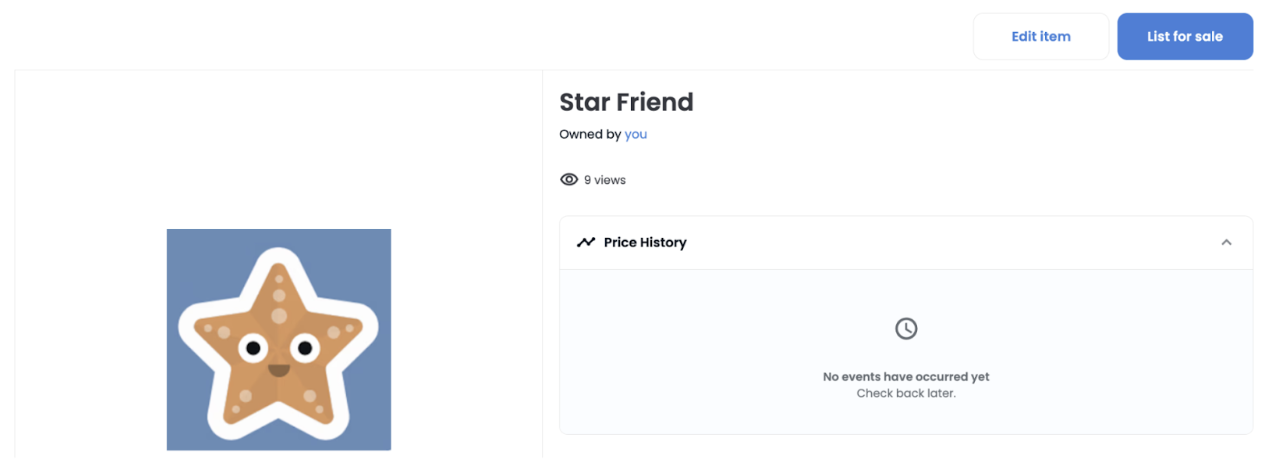

Selling NFTs in OpenSea

Here’s how to sell NFTs on OpenSea, a top platform for trading digital assets. OpenSea allows users to list and sell a wide variety of NFTs, providing options for setting prices and auction formats to maximize your sale.

- After connecting your wallet, go to your OpenSea profile by clicking your account icon and selecting the NFT you wish to sell from your collection.

- On the top right corner, click on “List for sale.”

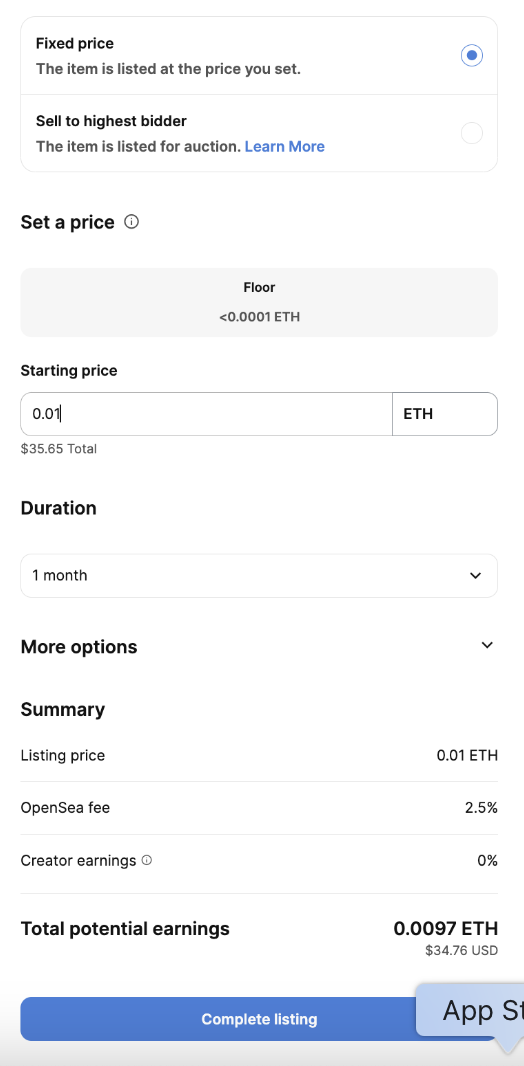

- Set the sale type, either as a fixed price or auction, and specify the price and duration.

- Review the listing details, then approve the transaction through your crypto wallet. Your NFT will now be available to users.

NFT Security and Concerns

Although NFTs seem very advantageous for those looking to make some profits in the digital market, they also come with some risks and concerns, and one of the main ones is piracy and copy issues. Even though NFTs establish ownership of a digital asset, they don’t prevent unauthorized copying or sharing of the asset. This means anyone can download or replicate the image or file associated with an NFT, even though they don’t own the tokenized version.

Sometimes, this replication can confuse potential buyers who imagine that owning an NFT means that they have complete control over it. Currently, marketplaces are working towards improving safety and originality regarding NFTs; however, piracy can still be an issue.

Another concern is that market volatility can also impact NFT transactions. The prices of the pieces may change depending on trends, demand, and sentiment. The value of an NFT can drop significantly if interest goes down as well, leaving buyers with assets they can’t sell at a profit or even recover their investment. This is especially risky for those who choose it as a long-term investment, as the market is new, relatively unregulated, and vulnerable to rapid shifts in popularity.

Lastly, environmental concerns can also be considered a downside of NFTs. Blockchain networks that use Proof of Work (PoW), such as Bitcoin, for example, require a considerable amount of energy. To address this issue, some projects use more eco-friendly systems, such as Solana or Polygon, or alternative consensus mechanisms that consume less power.

What Is the Difference Between NFT vs. SFT?

The main difference between NFTs (non-fungible tokens) and SFTs (semi-fungible tokens) is their fungibility. As we mentioned, NFTs are unique and cannot be exchanged one-to-one. On the other hand, SFTs are a hybrid between fungible and non-fungible tokens.

Semi-fungible tokens (STFs) are a kind of digital asset with fungible and non-fungible elements. Initially, SFTs function like fungible tokens—identical and interchangeable, meaning they can be exchanged or transferred just like standard tokens of the same type. However, once an SFT is redeemed, used, or transferred in a specific way, it becomes unique and behaves like a non-fungible token (NFT), holding distinct attributes or values.

A practical example of SFT technology is event tickets. Before the event date, these tickets are fungible, allowing buyers to trade or exchange them as identical assets. However, once a ticket is redeemed or after the event, each can transform into a unique digital item, serving as personalized proof of attendance. Similarly, items such as weapons or armor might initially be tradeable as identical assets in gaming. However, once a player customizes or uses an item, it becomes unique, embodying specific attributes or experiences tied to that player.

Key Difference

NFTs (Non-Fungible Tokens)

SFTs (Semi-Fungible Tokens)

Fungibility

Unique, not interchangeable

Initially fungible, later non-fungible

Use Case(s)

Collectibles, digital art, virtual real estate

Event tickets, in-game items, vouchers

Tradeability

Limited to specific marketplaces

More flexibility initially; varies post-use

ERC Token Standard

ERC-721, ERC-1155

ERC-1155

Supply and Flexibility

Limited, predefined; individual assets

Initially fungible with shared attributes; flexible post-use

The combination of NFTs and SFTs has brought several new and more efficient solutions to the blockchain ecosystem. By using both systems, developers can create more flexible ecosystems. For example, STFs can be used in gaming as in-game currencies, while NFTs represent exclusive skins or rare characters. This duality allows for more complex digital economies, enhancing user experience and broadening the potential applications of blockchain technology.

Future of NFTs: Trends and Potential

In the last few years, the NFT industry has expanded beyond its initial use in digital art and collectibles. In the gaming industry, for example, NFTs allow players to own, trade, and monetize virtual items like characters, skins, and land across platforms. Also, the integration with Metaverse features NFT plays a big role in creating virtual economies. Decentraland and Sandbox are some platforms supporting virtual real estate transactions as NFTs, allowing users to purchase, develop, and trade them with real-world value.

NFTs are also being applied outside the Metaverse in real-world scenarios. For example, brands and organizations are exploring NFT memberships, where ownership of a specific NFT grants access to exclusive events or benefits. Digital identities and verifiable credentials are also emerging use cases, allowing users to maintain a verified online presence or certifications via NFTs. This shift represents a broader application of blockchain technology, where NFTs serve as secure and verifiable representations of identity, property, or membership, blurring the line between the digital and physical worlds.

Now, regarding the issue of whether NFTs are a bubble or a long-term investment opportunity, experts are still divided. According to tech futurist Cathy Hackl, NFTs are evolving beyond art to offer real-world functionality, suggesting that, while individual assets may fluctuate, the underlying technology holds significant promise for the future. However, some skeptics insist that the high prices for some NFTs resemble speculative bubbles seen in past markets, with many assets potentially losing value as hype fades.

Final Thoughts on Non-Fungible Tokens

NFTs have quickly gained popularity and traction within the digital world. They symbolize a new way of viewing ownership and interaction with digital assets. They create new opportunities for decentralized ownership, community engagement, and secure digital identity verification.

As investments, NFTs are still a developing area, with some volatility as the market grows and matures. However, their growing applications in gaming, the Metaverse, and real-world contexts signal strong potential for sustained impact.

If you are interested in learning more about the future of NFTs, we recommend our exclusive interview with Roham Gharegozlou, CEO of Dapper Labs. In the interview, Gharegozlou discusses the evolving role of NFTs and how they’re expected to shape the digital landscape for years to come.

👉 Learn More: What Is Web3?

FAQs

Can you lose access to your NFT if the marketplace shuts down?

Can NFTs be stolen or hacked?

Do I need to know how to code to create an NFT?

Can I sell physical items as NFTs?

Are there any legal implications to owning an NFT?

2M+

250+

8

70

About Cryptonews

Our goal is to offer a comprehensive and objective perspective on the cryptocurrency market, enabling our readers to make informed decisions in this ever-changing landscape.

Our editorial team of more than 70 crypto professionals works to maintain the highest standards of journalism and ethics. We follow strict editorial guidelines to ensure the integrity and credibility of our content.

Whether you’re looking for breaking news, expert opinions, or market insights, Cryptonews has been your go-to destination for everything cryptocurrency since 2017.

Ryan Glenn

Ryan Glenn