Five Blockchain Use Cases Might Boost Global GDP by USD 1.76T – PwC

Driven by need for trust in digital world, blockchain technology is expected to boost global gross domestic product (GDP) by more than a trillion dollars, estimated professional services network PwC, and will do so through five major use cases.

PwC’s latest report, titled “Time for trust: The trillion-dollar reasons to rethink blockchain,” discussed the top five uses of blockchain driving its adoption, and their economic impact.

In the order of their potential to generate economic value, these use cases are:

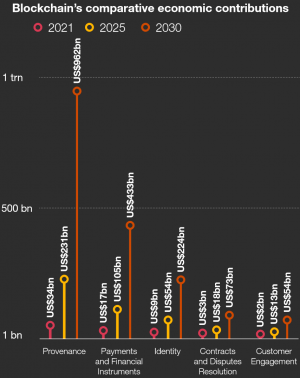

1. Provenance

Potential boost to global GDP by 2030: USD 962bn

Blockchain enables organizations and customers to track the movements of a product and identify its origin, and transparency allows for enhanced customer safety and trust, ethical responsibility, environmental friendliness, etc.

2. Payments and Financial Instruments

Potential boost to global GDP by 2030: USD 433bn

Wholesale central bank‑issued digital currencies (CBDCs) can facilitate more efficient clearing operations between central banks and their member banks, while retail CBDCs would be the digital equivalent of a bank note for public use. Meanwhile, stablecoins are used in experiments to transform cross border payments.

3. Identity

Potential boost to global GDP by 2030: USD 224bn

The new technology can safeguard personal credentials online, including personal identification and professional credentials and certificates, which would result in “vast” cost efficiencies and would help prevent fraud and identity theft.

4. Contracts and Dispute Resolution

Potential boost to global GDP by 2030: USD 73bn

Blockchain can bring great changes into this field, as it’s able to bring together ledgers, contracts, and payments, improving the flow of commercial agreements and flagging any disputes.

5. Customer Engagement

Potential boost to global GDP by 2030: USD 54bn

Blockchain can save traditional, card-based loyalty and reward programs from dying out, as it can boost engagement through integration with customer relationship management (CRM), as well as generate more value by making them more user-friendly for smartphone users.

This brings us to the report’s key finding, as it highlighted that,

“Blockchain technology has the potential to boost global gross domestic product (GDP) by USD 1.76 trillion [which is 1.4% of global GDP] over the next decade.”

This conclusion came from an assessment of the way in which the technology is being used at the moment, as well as its potential to “create value across every industry,” such as healthcare, government and public services, manufacturing, finance, logistics, and retail, found the PwC economists.

“There is an opportunity for all,” the report argued, adding that “our economists expect the majority of businesses to be using the technology in some form by 2025. Once it has hit the mainstream, the economic benefits are expected to rise steeply.”

Furthermore, PwC’s website enables users to observe the global economic impact of blockchain as it changes and grows each year until 2030, providing specific numbers for 12 individual countries and ‘rest of the world,’ by total blockchain impact or specific use case.

Looking at total blockchain impact in 2021, PwC estimates it to be USD 65.8bn, with United States’ USD 15.1bn at the top, followed by China’s USD 13.1bn, and then Germany’s USD 3.8bn. The rest of the world combined brings in nearly USD 21bn. However, by 2022, this number will have more than doubled to USD 138.9bn.

In 2025, the number is USD 422bn. China has overtaken the US by 0.2bn, Germany is still third, and several other countries have joined the double-digit team. In 2028, the number is up to 1046.1bn, with the US back in the leader position. Finally, in 2030, we see that talked-about USD 1.76tn additional value created by blockchain. China’s USD 440.4bn leads; the US is second with USD 407.2bn, and Germany is third with USD 95.3bn. The rest of the world combined, besides the mentioned 12 countries, brings in USD 473.3bn.

Meanwhile, a software engineer at crypto market data provider Messari, Jonathan Otto, argued that the value of blockchain is that people don’t need to trust a third-party human or organization, but a code which they themselves can read.

“This means I didn’t need to trust a company or a government to save me. If I was confident the code worked, then I could be confident that my money was safe. This is why blockchains matter,” wrote Otto.

Otto said that evaluating blockchain technology objectively allows one to see it’s possible to “engineer a blockchain network with whatever properties we need to replace legacy assets from first principles,” adding: “The question is not: “is crypto asset $XYZ correlated with stocks?”. The right question is “is crypto asset $XYZ engineered to be correlated with stocks?”.”

However, despite the estimated strong growth by PwC, a separate recent report showed that blockchain is now used by a number of companies that do not have clearly defined problems they claim to have solved with the novel technology. Also, nearly half of the examined companies showed no evidence of a problem solved.

____

Learn more:

Bitcoin Is Blockchain’s ‘Killer App,’ But Blockchain Is Catching Up

How Blockchain Will Help Send People Into Space

Crypto ‘Is Now Finally Being Taken Seriously’ By Taxman – PwC

- Perplexity AI Predicts XRP Will Hit This XRP Price by End of 2026

- Microsoft Copilot AI Predicts Insane XRP Price by End Of 2026

- Sam Altman ChatGPT AI Predicts Insane SpaceX Stock Price by End of 2026

- Google Gemini AI Predicts Shocking Bitcoin Price by End of 2026

- Ripple Crowned: UK Treasury Just Changed Everything for XRP

2M+

250+

8

70

- Perplexity AI Predicts XRP Will Hit This XRP Price by End of 2026

- Microsoft Copilot AI Predicts Insane XRP Price by End Of 2026

- Sam Altman ChatGPT AI Predicts Insane SpaceX Stock Price by End of 2026

- Google Gemini AI Predicts Shocking Bitcoin Price by End of 2026

- Ripple Crowned: UK Treasury Just Changed Everything for XRP

More Articles