China Changes its Stance Towards Bitcoin Mining

China’s state planner, the National Development and Reform Commission (NDRC), has reportedly removed Bitcoin (BTC) mining from the list of industries that might be eliminated.

Cryptocurrency mining has not been included in the finalized catalog for Guiding Industry Restructuring that will take effect from Jan 1, 2020, per Coindesk. The catalog was published today.

As reported in April, the Commission was seeking public opinions whether Bitcoin mining should be immediately banned. Bitcoin mining was included in a draft list of industrial activities the agency was seeking to stop, as they did not adhere to relevant laws and regulations, were unsafe, wasted resources or polluted the environment.

In either case, despite all efforts to push Bitcoin miners out of the country, Bitcoin mining was never officially illegal in China.

Su Zhu, CEO of Singapore-based investment management firm Three Arrows Capital, reacted by saying that he wouldn’t be surprised if “mining becomes designated a strategically important activity at some [point].”

The announcement today comes hot on the heels of the recent urge by China’s President Xi Jinping to accelerate the development of blockchain technology due to its importance “in the new round of technological innovation and industrial transformation” of China.

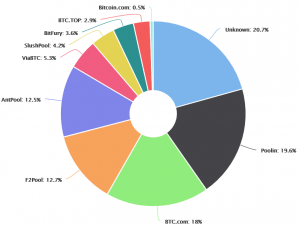

Chinese miners are already major players in the Bitcoin mining industry. For example, at the time of writing, four largest mining pools (Poolin, BTC.Com, F2Pool and AntPool) are from China and hold almost 63% of the Bitcoin network hashrate, which essentially measures how much computing power is needed to maintain the network.

Bitcoin hashrate distribution

In either case, there are concerns that China holds more influence over Bitcoin than many are ready to admit.

China “threatens the security, stability, and viability of Bitcoin” with its “political and economic control over domestic [cryptocurrency] activity, and control over its internet infrastructure,” a study, published in October 2018, from Princeton and Florida International Universities claimed.

“In theory it’s possible for a government to launch a 51% attack. If a government like the US or China decided they wanted to hurt Bitcoin, they could either rapidly shut down a lot of mining power so that they control a majority of what’s left, or they could deploy new hashpower that takes over the network,” Prof. Matthew Green of John Hopkins University told Cryptonews.com earlier this year. However, he doesn’t regard a 51% attack on Bitcoin as especially likely though, due to the enormous expense involved.

“The thing to keep in mind is that 51% attacks, while they’re terrible and undermine confidence, basically just allow double spending,” says Green. “This is really bad for merchants and exchanges, and in the long run it could make Bitcoin unusable. But it doesn’t allow the attacker to, say, steal everyone’s coins. And the cost of a rollback goes up as you go farther back in time.”

Meanwhile, in 2018, articles from influential state-run Chinese media outlets signaled that further crackdowns could be launched to force out remaining cryptocurrency trading and mining activities from the country. However, until now, miners have shown a surprising resilience.

Nonetheless, many of those mining companies were looking to relocate to more favorable locations overseas such as Iceland, Canada, and the US, to name a few.

At pixel time (07:11 UTC), BTC trades at c. USD 9,410 and is up by 1.45% in the past 24 hours and by 1.47% in the past week.

- Elon Musk Grok AI Predicts Shocking XRP Price by End of 2026

- Sam Altman ChatGPT AI Predicts Stunning Bitcoin Price By End Of 2026

- XRP Price Prediction: Ripple Taps Indonesia, Philipines, and Vietnam Market

- Bitcoin Price Prediction: BTC Eyes Upside as Franklin Templeton Pushes Stock Dividends

- Crypto News, June 23: Why is Crypto Down? BTC USD Falls Under 63K, as ETH Hits Triple Bottom in Massive Leverage Flush

2M+

250+

8

70

- Elon Musk Grok AI Predicts Shocking XRP Price by End of 2026

- Sam Altman ChatGPT AI Predicts Stunning Bitcoin Price By End Of 2026

- XRP Price Prediction: Ripple Taps Indonesia, Philipines, and Vietnam Market

- Bitcoin Price Prediction: BTC Eyes Upside as Franklin Templeton Pushes Stock Dividends

- Crypto News, June 23: Why is Crypto Down? BTC USD Falls Under 63K, as ETH Hits Triple Bottom in Massive Leverage Flush

More Articles