Bitcoin Option Markets Signal Upside Price Risk Despite Warnings of Possible Fed-fuelled Sell-off

Bitcoin options markets continue to signal near-term upside risks to the BTC price, despite warnings from strategists that Wednesday’s Fed meeting could trigger a “bloodbath” in cryptocurrency markets.

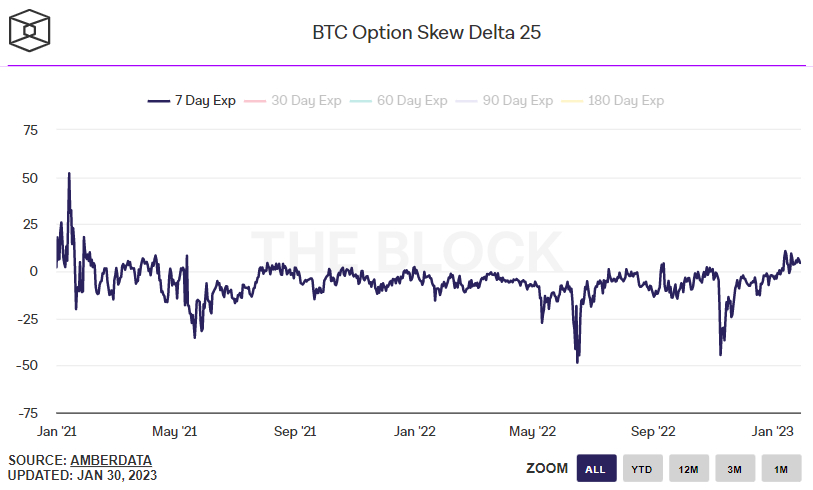

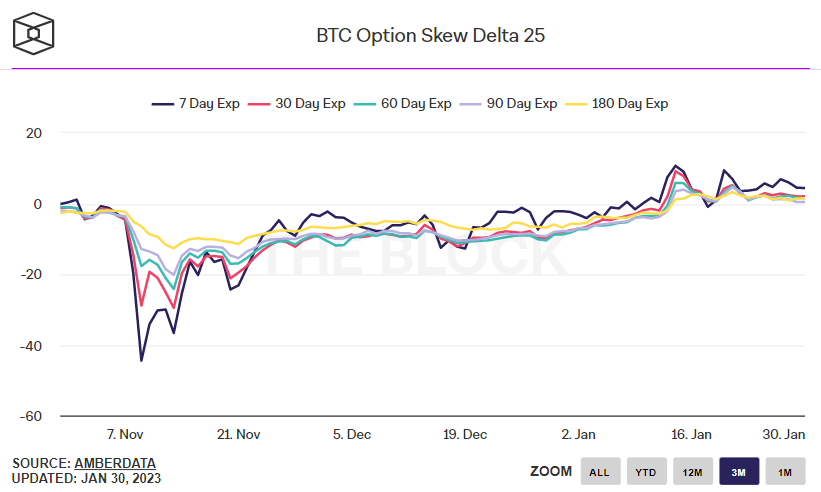

According to a chart on The Block, the widely followed 25% delta skew of Bitcoin options expiring in seven days remained at 4.44 on the 30th of January, not too far below recent multi-year highs hit earlier this month in the 9.0 area. The 25% delta skew of Bitcoin options expiring in 30, 60, 90 and 180 days were all between 0.5 and 2.0, indicating more of a neutral market bias, though all also remain close to multi-month highs.

The 25% delta options skew is a popularly monitored proxy for the degree to which trading desks are over or undercharging for upside or downside protection via the put and call options they are selling to investors. Put options give an investor the right but not the obligation to sell an asset at a predetermined price, while a call option gives an investor the right but not the obligation to buy an asset at a predetermined price.

A 25% delta options skew above 0 suggests that desks are charging more for equivalent call options versus puts. This implies there is higher demand for calls versus puts, which can be interpreted as a bullish sign as investors are more eager to secure protection against (or bet on) a rise in prices.

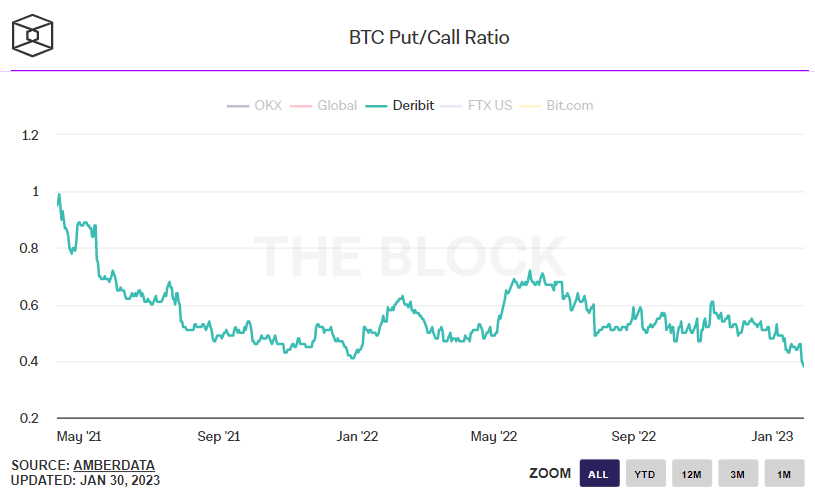

Elsewhere, the Bitcoin Open Interest Put/Call Ratio on dominant crypto derivatives exchange Deribit on the 29th of January slumped to a new record low at 0.38. That means that investors favour owning call options (bets on the price rising) over put options (bets on the price dropping) by a record margin.

Fed Meeting Might Trigger Crypto “Blood”

The Fed is widely expected to raise interest by a further 25 bps on Wednesday, taking the Federal Funds Target Range to 4.50-4.75%. A 25 bps rate hike will thus come as no surprise and shouldn’t move markets at all. What matters to markets is the outlook for interest rates.

More specifically, how many more rate hikes will there be? And how long will interest rates be held at the restrictive terminal rate? Markets seem to be taking the view that, after Wednesday’s hike, the Fed will only lift interest rates by 25 bps one more time (in March) and will then start cutting interest rates in late 2023.

That seems to be based on the bet that 1) US inflation (price and wage pressures) will continue to slump back towards the Fed’s 2.0% target and 2) the US will enter a recession later this year – meaning the Fed will have the room and desire to start cutting interest rates to support the economy.

But strategists are warning that markets are underestimating the Fed’s resolve to raise interest rates and hold them at restrictive levels for longer. According to popular pseudonymous macro-focused Twitter account The Carter, the Goldman Sachs US Financial Conditions Index (FCI) is now at its lowest level since September 2022.

The Goldman Sachs US FCI is now solidly below the December level that prompted the re-tightening barrage. pic.twitter.com/vMB8lZavnX

— The Carter (@TheCarter758) January 27, 2023

The Carter thinks that, as a result, “there will be blood on February 1”, with Fed Chairman Jerome Powell to “re-tighten financial conditions by forcefully addressing rate cuts (i.e. bets on rate cuts)… head-on”.

There will be blood on February 1.

— The Carter (@TheCarter758) January 27, 2023

Powell will re-tighten financial conditions by forcefully addressing rate cuts head-on.

“The Powell Fed is laser-focused on not “prematurely easing” policy to avoid the Burns Fed “stop and go” error,” The Carter continued, adding that “the mere discussion of rate cuts is anathema” to the Fed’s broader tightening project.

A violent upwards repricing of the Fed’s interest rate intentions over the coming year (perhaps markets are forced to price interest rates moving and staying above 5.0% for the remainder of the year) would likely trigger a big move higher in the US dollar, US bond yields and downside in assets like stocks, gold and crypto.

But Options Markets Don’t Seem to Concerned About Potential Volatility

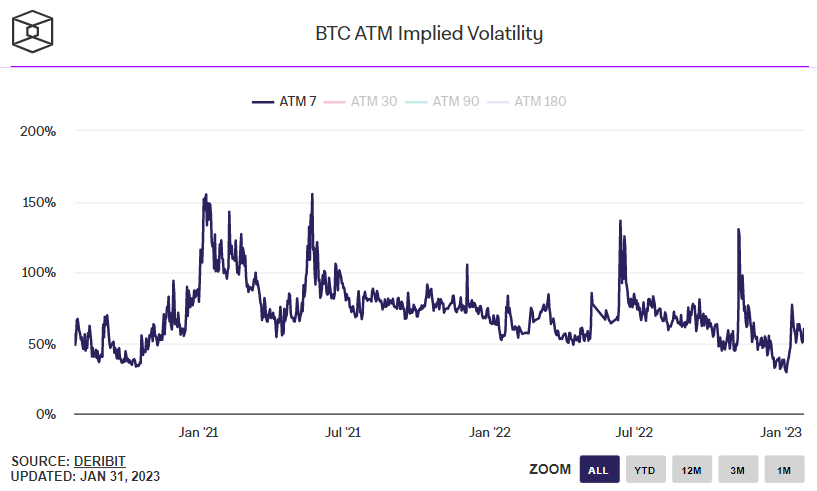

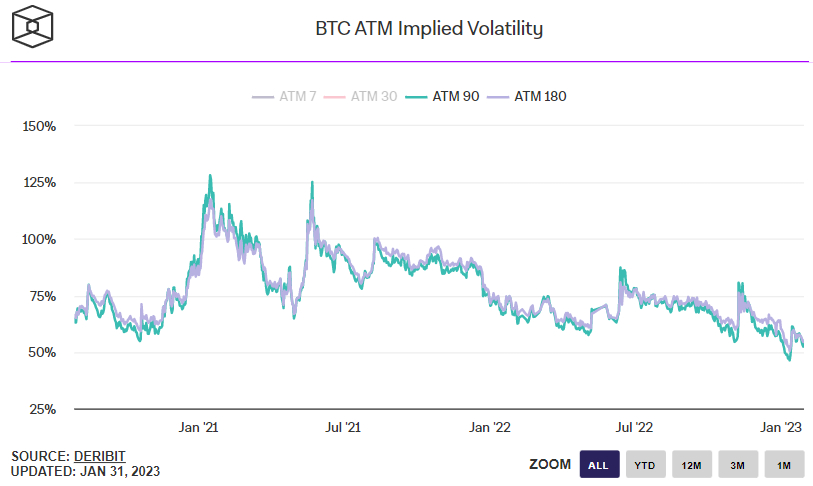

Despite dire warnings of an imminent potential pullback in the BTC price, options markets also don’t seem too concerned about an uptick in volatility. At the money (ATM) Implied Volatility of options expiring in seven days’ time was last around 60%, roughly in line with where it has been since the middle of January and still below its average level for 2022 and 2021, though still substantially up from record lows printed earlier this month under 30%.

Options expiring in 90 and 180 days’ time both continue to signal that expectations about Bitcoin’s longer-term volatility remain close to record lows.

That may be because, despite the risk that the Fed causes ructions this week, Bitcoin investors appear to be growing more confident that 2022’s bear market is over. As covered in a recent article, six out of eight indicators watched by analysts at crypto data analytics platform Glassnode to identify when Bitcoin is transitioning out of a bear market are flashing bullish signals, and a seventh is likely to also soon turn green.

- Bitcoin Price Prediction: Saylor’s Strategy is a Risk to Bitcoin, According to JP Morgan

- Elon Musk Grok AI Predicts Incredible XRP Price and Bitcoin Price by End of 2026

- Mark Zuckerberg’s Meta AI Predicts Unbelievable Bitcoin Price by the End of 2026

- Sam Altman ChatGPT AI Predicts Massive Meta Platforms Stock Price Surge by 2026

- XRP Price Prediction: Volume and ETF Inflow Send Ripple Token Higher

2M+

250+

8

70

- Bitcoin Price Prediction: Saylor’s Strategy is a Risk to Bitcoin, According to JP Morgan

- Elon Musk Grok AI Predicts Incredible XRP Price and Bitcoin Price by End of 2026

- Mark Zuckerberg’s Meta AI Predicts Unbelievable Bitcoin Price by the End of 2026

- Sam Altman ChatGPT AI Predicts Massive Meta Platforms Stock Price Surge by 2026

- XRP Price Prediction: Volume and ETF Inflow Send Ripple Token Higher

More Articles