CBDCs Are Under Threat — Here’s Why

Key takeaways:

- CBDCs have struggled with low adoption rates despite years of development and testing.

- Some countries, like Australia and Canada, have stopped plans to launch CBDCs due to low public interest.

- The IMF suggests central banks improve communication and offer incentives, such as sign-up bonuses, to increase CBDC adoption.

The world of central bank digital currencies is in disarray right now.

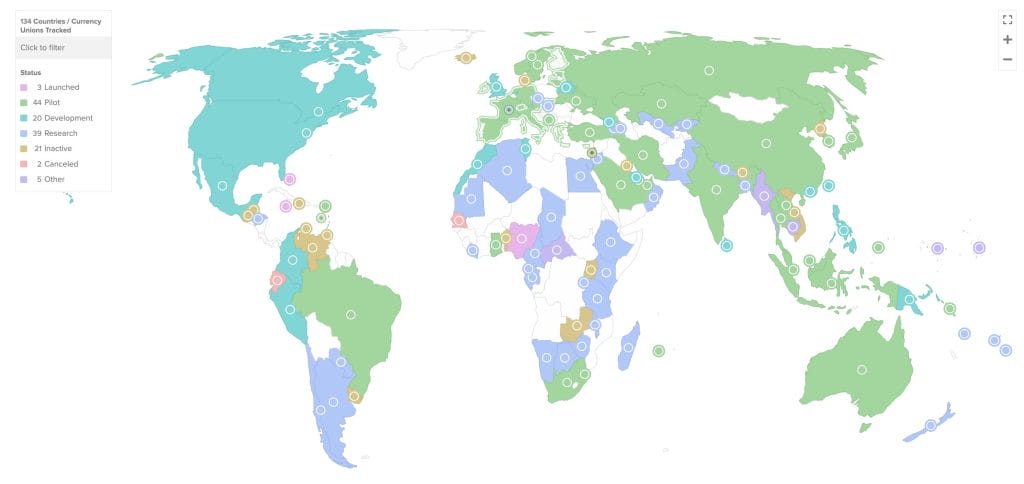

Just three CBDCs have officially launched worldwide, while another 44 are in the pilot stage.

That’s according to the Atlantic Council, which has long tracked their evolution globally.

Those that have made their debut have often faced disappointing levels of adoption — primarily because consumers are stuck in old habits and reluctant to make a change.

Over in The Bahamas, just 1% of currency in circulation is denominated in “The Sand Dollar,” the name given to its CBDC.

As a result, regulations are being pushed through that will force banks in the region to offer this digital asset to their customers.

There hasn’t been much success in Nigeria either, with uptake of the eNaira largely linked to cash shortages that caused widespread protests in major cities.

And over in Jamaica, there was an embarrassing development when the CEO of National Commercial Bank — the only financial institution that offers JAM-DEX — said usage of this CBDC had been “low” and caused friction compared with existing methods.

Other central banks are now openly questioning whether consumers have much demand for retail CBDCs, with both Australia and Canada abandoning plans to launch one. Meanwhile, the Federal Reserve remains in a state of paralysis in its deliberations on whether to develop a digital dollar. North Carolina has banned this CBDC altogether even though it doesn’t even exist yet — with politicians fearful it could be used to control how consumers spend their money.

This mixed picture is sending regulators and central banks back to the drawing board — leading to a flurry of chin-scratching papers that examine how to encourage consumers to embrace digitized fiat currencies, and prevent low levels of adoption after launch.

IMF: ‘Slow Uptake’ So Far

A recent report by the International Monetary Fund painfully set out the missteps made by first movers so far — and admitted that it isn’t easy to scale up new CBDCs. But the authors believe this doesn’t mean such digital assets are failures, adding:

“Multiple barriers to adoption may stand in the way, such as a lack of public awareness and trust, privacy protection concerns, preference for existing instruments, and lack of appropriate incentives for attracting intermediaries.”

This is a succinct precis of the challenges that central banks are facing. CBDCs aren’t often talked about in the news, meaning consumers might not have a clue they exist. Among those who have heard about this technology, some will have been concerned by critics who claim governments may snoop on their transactions. It’s also fair to say that some central banks haven’t done a good enough job of ensuring CBDCs are better than cash or cards — and offer something that well-established payment methods do not.

To compound the problem, financial institutions aren’t happy either. They’re worried that their business models could erode overnight — with consumers holding their deposits with central banks instead of them. That, in turn, could affect their ability to lend, which, in a worst-case scenario, could make it much harder to secure a mortgage.

The IMF went on to argue that central banks must do a better job of communicating with all stakeholders — whether that’s merchants, consumers or banks — about their ambitions for a CBDC and what it would mean for them. That involves “identifying their needs and pain points, as well as social and cultural factors that influence their financial behavior.”

But much more than that, the Fund said the design of digital currencies matters too — as well as incentives so businesses and shoppers are keen to get involved. That could include the monetization of anonymized CBDC data for merchants, along with “sign-up bonuses, airdrops or lotteries” for the public.

Why is Demand So Low?

Over at the European Central Bank, where work is well underway to unveil a digital euro, researchers argued that policymakers haven’t spent enough time reflecting on how the arrival of CBDCs would affect consumers, writing:

“Introducing a novel payment method presents an inherent “cost” to consumers, and this is not purely a monetary cost — it also encompasses the effort, time and adjustments required of consumers when adapting to a new payment method.”

The authors went on to say that the chances of a successful launch would be boosted if the digital euro is fully customized around the needs of everyday shoppers — complete with an information campaign that clearly sets out the benefits of this new asset.

“Our study suggests that CBDC demand could be influenced by merging the perceived top qualities of cards (like speedy transactions and ease of use) with the benefits of cash (such as tracking expenses and preserving privacy.)”

Research by Positive Money Europe went on to claim that the ECB is “heeding to the bank lobby and baking their interests into the design of a digital euro” — and that is ultimately undermining the CBDC’s appeal at a time when it is badly needed.

The damning report went on to argue that a rising number of merchants refusing to accept cash means consumers are missing out on anonymous payment methods — and to make matters worse, 13% of residents within the eurozone don’t have a debit or credit card. All of this comes as the fees charged by Mastercard and Visa continue to rise, with many businesses passing on this expense to shoppers still feeling the effects of the cost-of-living crisis.

What Happens Next?

Economies around the world have been keeping a very close eye on The Bahamas, Jamaica and Nigeria — taking notes based on where things have gone wrong.

Meanwhile, it’s interesting to see the likes of China has been slow and methodical in the pilot programs for their CBDC. Tests have been going on for years, with this digital asset gradually rolled out to new cities. This has been combined with specific use cases that center on tuition fees, public transport and taxation.

With plenty of challenges left to resolve, the next couple of years will be pivotal if CBDCs are going to become a mainstay in 21st-century finance. As things stand, many major economies may end up concluding that they’re simply not worth the effort.

- Dario Amodei Claude AI Predicts the Next Chapter for Bitcoin in 2026

- Elon Musk Grok AI Predicts XRP Could Be Gearing Up for Something Big

- Google Gemini AI Predicts a Bitcoin Price Swing Nobody Is Pricing In

- XRP ETF Inflows Have Collapsed 79% Since May as the CLARITY Act Stalls, Is $1 About to Break?

- The Senate Just Shelved the CLARITY Act, And JPMorgan Says Crypto’s Tokenization Boom Could Slip Away to Wall Street

2M+

250+

8

70

- Dario Amodei Claude AI Predicts the Next Chapter for Bitcoin in 2026

- Elon Musk Grok AI Predicts XRP Could Be Gearing Up for Something Big

- Google Gemini AI Predicts a Bitcoin Price Swing Nobody Is Pricing In

- XRP ETF Inflows Have Collapsed 79% Since May as the CLARITY Act Stalls, Is $1 About to Break?

- The Senate Just Shelved the CLARITY Act, And JPMorgan Says Crypto’s Tokenization Boom Could Slip Away to Wall Street

More Articles