Clend Review 2026

Clend Review 2026

- Excellent way to unlock your crypto's value without selling

- Low APR compared to market rates

- Straightforward borrowing terms

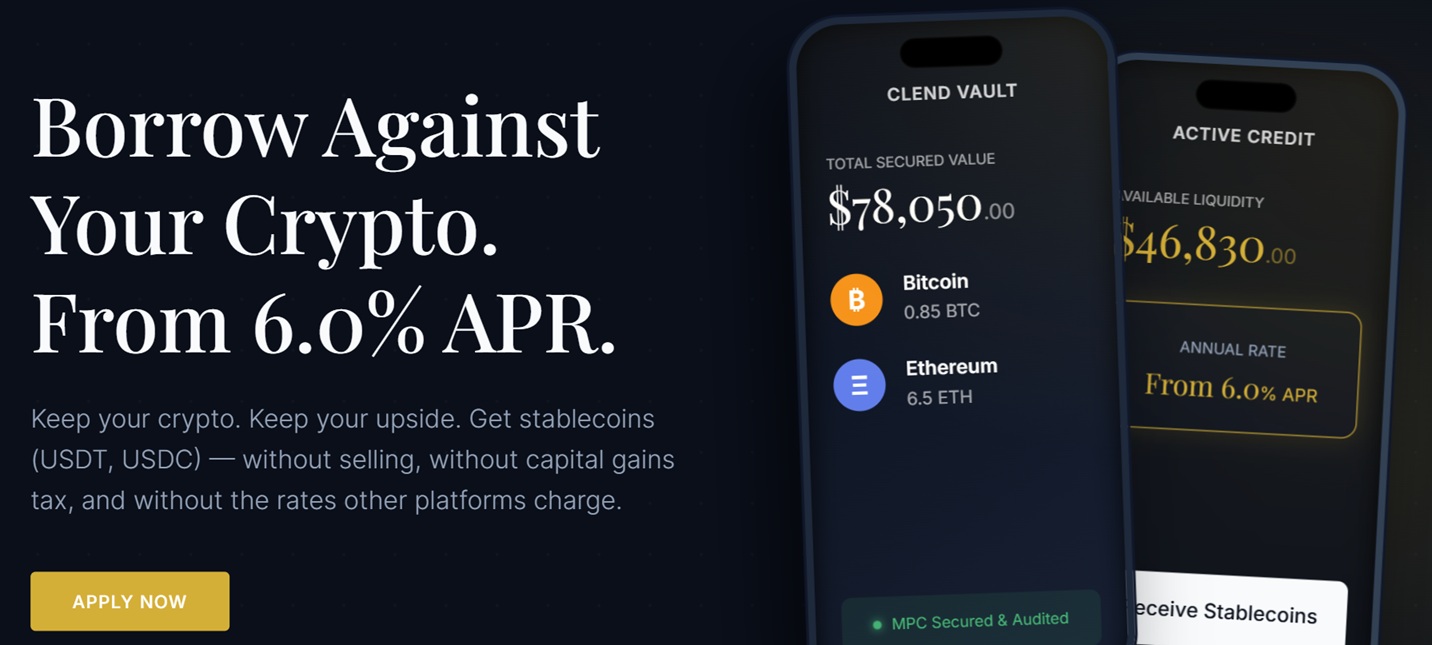

Crypto holders sitting on large unrealized gains face a familiar trap: if you start accessing the value, for instance, selling your crypto, you usually trigger a taxable event. Clend offers an alternative path – letting you take out collateralized loans against around 20 cryptocurrencies, with loans provided in stablecoins, with no monthly payment requirement, and no need to touch the underlying position.

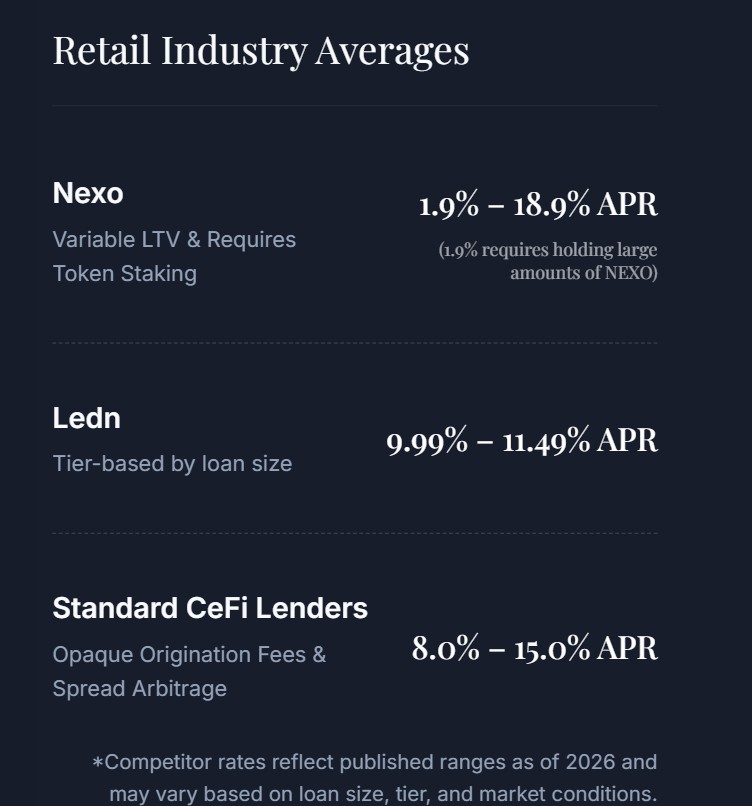

Loans can start at around 30,000 USDC and offer APRs starting from 6.0% (on BTC) and ranging up to 16.80% – the industry average is around 15%, so the best rates on Clend are beyond comptitive.

Our Clend review covers how the service works, its pros and cons, ease of use, how to use the platform, the benefits of borrowing against your assets rather than selling your crypto, and any risks to consider before you start.

About Clend

Clend is a crypto-backed lending service operated by R0 Inc., a U.S.-based entity headquartered in New York City. The service is available in English and Japanese, with a dedicated site for the Japanese market, where the tax efficiency angle is particularly prominent – crypto gains in Japan are currently taxed at up to around 55%.

Clend’s core service is easy to understand – you deposit crypto as collateral, receive stablecoins (USDT or USDC), keep ownership of the underlying asset, and repay in full when ready.

Because your crypto is pledged rather than sold, no disposal event occurs at the time of borrowing (in many jurisdictions), so no capital gains are recognized. Tax treatment always depends on individual circumstances and local regulations, so it is worth understanding how this applies to you specifically.

The service accepts both individual and corporate borrowers, though we sense that Clend lends itself (no pun intended) more towards high-net-worth individuals and Web3 companies using crypto treasuries for working capital or growth funding. For example, the minimum collateral required is approximately 33,000 USD.

How Clend Works

As an overcollateralized lending mode, Clend’s system is closer to a pawn-style model than a traditional loan. Assets are held in custody and never lent out or rehypothecated. That structure, in which Clend holds collateral rather than deploying it, is what Clend cites as the reason it can offer rates starting at 6.0% APR. There is no fractional-reserve lending, no rehypothecation exposure, and no spread arbitrage added on top.

Security is handled through Fireblocks, the institutional-grade custody infrastructure used by major financial institutions globally. Specifically, Clend uses Fireblocks’ MPC-CMP technology (multi-party computation) combined with hardware security modules (HSMs).

The private keys are generated and stored in the HSMs; the MPC model eliminates any single point of failure. Fireblocks’ infrastructure is SOC 2 Type 2 compliant and subject to regular third-party audits.

The interest model is unique among lending services, as there are no monthly payments. Instead, Unpaid interest is automatically added to the loan balance. The borrower settles everything (principal plus accumulated interest) when they repay, with full repayment available from day 61 onward.

Liquidation is balance-based, not price-based, with the trigger being the loan balance (principal plus accrued interest) reaching 90% of the collateral’s current value (95% for stablecoin collateral). So a sudden market drop does not automatically trigger liquidation; what matters is whether the growing loan balance approaches that threshold.

Adding collateral at any point reduces the LTV and pushes the liquidation point further away.

Pros

- No taxable disposal event at point of borrowing, though users should consult a tax professional for their specific circumstances

- No monthly payment; interest compounds into the balance and is settled at repayment

- Rates start at 6.0% APR for BTC with no platform token requirement

- Higher LTV than competing services on BTC, ETH, XRP, and SOL

- Collateral held via Fireblocks MPC, providing institutional-grade custody with SOC 2 Type 2 compliance

- Balance-based liquidation means a short dip alone does not trigger loss of collateral

- Same-day disbursement is possible after collateral deposit is confirmed

- Available to both individuals and corporate borrowers

- No hidden fees, no origination fees, and no prepayment penalties

Cons

- Minimum loan of 30,000 USDC, approximately ¥5,000,000, with minimum collateral of approximately 33,000 USD equivalent

- Loan term is capped at 12 months

- Collateral can still be liquidated if LTV reaches the threshold

- Tax treatment is not guaranteed and varies by jurisdiction

Services & Rates

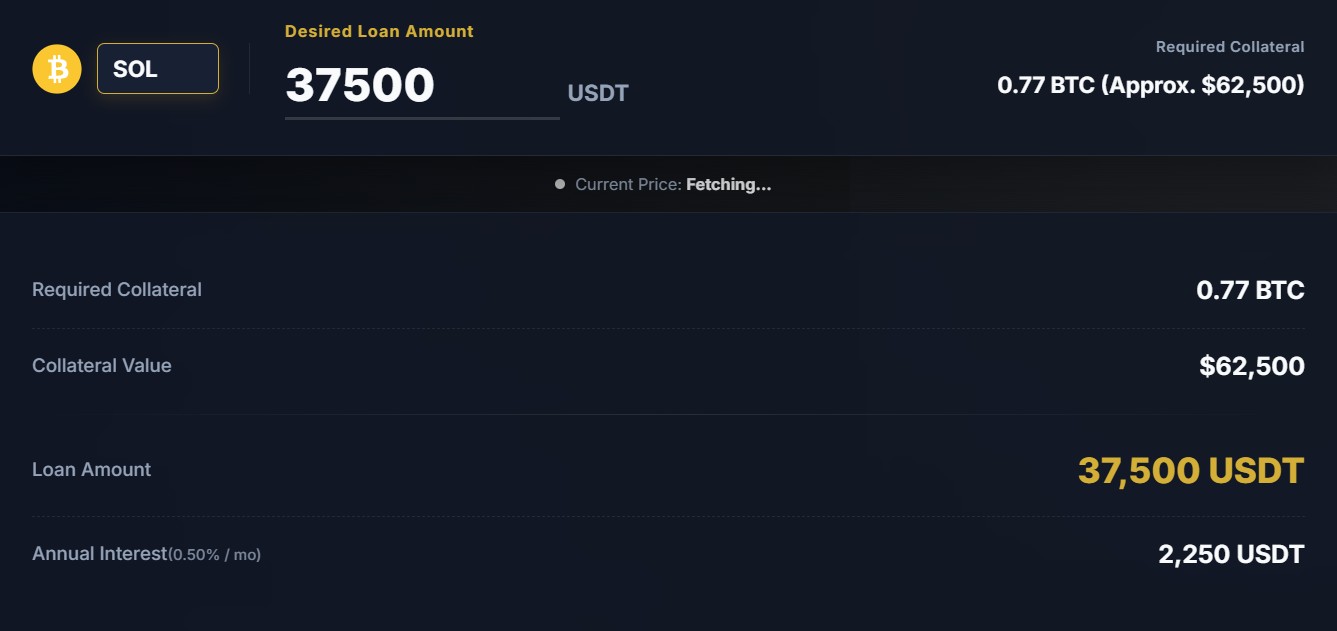

Clend accepts 19 collateral assets, with rates and LTVs tiered by asset quality, and the best terms on the largest cap coins. Some examples (rates correct as of June 2026):

| Tier | Examples | LTV | Liquidation LTV | Rate (per year) |

| Stablecoins | USDC, USDT, JPYC | 90% | 95% | 14.40% |

| Major | BTC | 60% | 90% | 6.00% |

| Major | ETH | 60% | 90% | 7.20% |

| Altcoins | XRP, SOL | 40% | 90% | 8.40% |

| Altcoins | BNB, ADA, DOGE, SHIB, MATIC, etc. | 40% | 90% | 16.80% |

The annual rates shown are nominal (monthly rate multiplied by 12) and because interest compounds monthly into the balance, the effective annual rate may be modestly higher. Clend calculates interest on a full-month basis – no daily proration – which is worth factoring in on shorter borrowing windows.

The liquidation LTV for most assets is 90% of the loan balance, meaning the outstanding amount (principal plus accumulated unpaid interest) must reach 90% of the collateral’s current market value before liquidation is triggered. For stablecoins the threshold is 95%.

As an example: 1,000,000 JPY of ADA collateral borrowed against at 40% LTV produces a 400,000 JPYC loan. Liquidation triggers when the balance – growing each month as interest compounds – reaches 90% of whatever the ADA is then worth. Topping up collateral at any point resets the percentage.

Loans are USDT and USDC (and JPYC for the Japanese market) across multiple networks: ERC-20, BSC, TRON, Polygon, and Omni for USDT; ERC-20 for USDC; and native chains where applicable.

Clend’s rates are fixed and require no token holding.

Who Is Clend For?

Clend’s minimum loan size and collateral floor put it firmly in the institutional and high-net-worth segment. The service is explicitly not designed for someone with a few hundred dollars of ETH who needs additional money.

So the clearest use case is likely a long-term BTC or ETH holder facing a large near-term cash need – a tax bill, a real estate deposit, a business opportunity – who does not want to dispose of their position. Selling a large BTC holding creates an immediate capital gains event in most places in the world, and permanently forfeits future upside on the sold portion. A collateralized loan at 6.0% APR can avoid both.

The second natural use case is Web3 companies and crypto-native corporates sitting on treasury assets. Using BTC or ETH holdings as collateral to fund operating expenses or growth capital keeps the balance sheet intact and avoids realizing gains.

Clend is probably not the right service for someone who might need to exit the position quickly as the 61-day lock on full repayment, and the 12-month maximum term mean borrowers need a reasonably clear repayment horizon before signing.

How to Use Clend

The process runs entirely online in four stages – and before you start, you can try out the on-site calculator to see your potential loan.

Step 1 – Application: Submit the application form at icoalert.com. The team reviews the collateral and prepares a personalized loan plan.

Step 2 – KYC: Identity verification is completed online. The KYC requirement applies regardless of whether the borrower is an individual or a corporate entity.

Step 3 – Contract: Loan terms are reviewed and the agreement is signed digitally. This covers the loan amount, interest rate, collateral asset, and the 12-month term.

Step 4 – Collateral deposit and disbursement: Once the collateral is transferred to the designated Fireblocks-secured address and the blockchain confirmation is received, stablecoin funds are sent.

Clend states this can happen the same day in many cases, though the timeline will depend on confirmation speed for the collateral asset and when procedures are finalized.

There are no origination fees, no withdrawal fees on the disbursed funds, and no prepayment penalties. The only cost is the stated interest rate.

Is Clend Worth Using?

For the right user, the value proposition is excellent. A BTC holder who needs six figures in stablecoins for 6 to 12 months, who doesn’t want to trigger a capital gains event, and can comfortably manage the downside of a potential liquidation can get a fixed 6.0% APR, same-day funding, institutional custody, and no monthly cash flow drain. It is a specific but legitimate use case, and the rate is competitive for a fixed, no-token-required CeFi product.

We’ll point out the compounding interest structure. Because there are no monthly payments, the loan balance grows each month automatically, so a BTC loan at 0.50% monthly sounds modest, but over 12 months at full term with no partial repayments, the effective annual cost will be just above the 6.0% – and more importantly, the growing balance continuously pushes the LTV closer to the 90% liquidation threshold. Those terms make sense, but we think they are worth highlighting.

The minimum entry point (approximately 33,000 USD in collateral) may make Clend less accessible to the average retail crypto holder, but for those who qualify, Clend solves a real problem.

Conclusion

Clend does one thing extremely well: it lets crypto holders borrow stablecoins against their holdings without having to sell them, reducing the likelihood of a tax event in many cases.

The rate structure is transparent and fixed, collateral is secured via Fireblocks MPC, and the no-monthly-payment model suits borrowers who prefer to settle at term rather than manage cash flow each month.

We appreciate how easy it is to get started, the clear and transparent terms on offer, and Clend is another excellent example of how crypto changes how we can use our money.

If you are the right user, Clend makes a lot of sense.

Legal notices:

Clend is operated by R0 Inc. (U.S.-based entity). The service is not subject to Japan’s Financial Instruments and Exchange Act or crypto asset exchange business registration requirements. Digital asset prices are highly volatile. Collateral can be liquidated at set LTV thresholds. Tax treatment varies by jurisdiction and individual circumstances; consult a qualified tax professional. This article does not constitute financial, investment, or legal advice.

FAQs

What is Clend?

What is the minimum loan amount on Clend?

How does liquidation work on Clend?

Does Clend require monthly payments?

Is borrowing against crypto a taxable event?