Crypto Taxes Explained in July 2026

- In This Article

-

- Profitable Crypto Investments

- Trading Cryptocurrencies

- Earning Crypto Income on DeFi Investments

- Paying for Goods or Services With Crypto

- Crypto Mining

- Selling Goods for Crypto

- Unprofitable Crypto Investments

- Receiving a Salary in Crypto

- Donating Crypto

- Gifting Crypto

- Trading Stablecoins

- Trading NFTs

- Airdrops, Hard Forks, and Token Rewards From DAOs

- Crypto as Part of an Inheritance

- In This Article

-

- Profitable Crypto Investments

- Trading Cryptocurrencies

- Earning Crypto Income on DeFi Investments

- Paying for Goods or Services With Crypto

- Crypto Mining

- Selling Goods for Crypto

- Unprofitable Crypto Investments

- Receiving a Salary in Crypto

- Donating Crypto

- Gifting Crypto

- Trading Stablecoins

- Trading NFTs

- Airdrops, Hard Forks, and Token Rewards From DAOs

- Crypto as Part of an Inheritance

Show Full Guide

The Internal Revenue Service (IRS) treats digital assets as property, meaning they’re taxed similarly to stocks and other capital assets. Similar to tax treatment for stocks, crypto taxes fall into one of two categories: capital gains or income.

This guide on crypto tax explains when taxes apply, and which types apply to specific types of crypto transactions. We’ll cover capital gains and income requirements, as well as what rates to expect and how to keep your tax liabilities to a minimum.

Key Takeaways on Crypto Taxes

The key takeaways on crypto tax in the US are as follows:

- The IRS views crypto assets as property, so they’re taxed the same as stocks, ETFs, and similar investment classes.

- Capital gains tax is assessed on realized profits, meaning you need to pay tax only if you sell your crypto for more than you bought it. Losses reduce taxable gains, and tax rates depend on whether the crypto assets were held for under or over 12 months.

- The IRS will also tax crypto income, such as staking and yield farming rewards, upon receiving them.

- For the 2026 tax year, the standard deduction for a single filer is $16,100.

- The IRS ended the “universal” cost base method for digital assets. Starting Jan. 1, 2025, all taxpayers must switch to the per-wallet or per-account cost-tracking method.

- Beginning Jan. 1, 2025, centralized exchanges and brokers must report the gross proceeds from crypto sales and exchanges on a new tax form – 1099-DA. Beginning with the 2026 tax year, Form 1099-DA will also include cost basis information.

- There are several ways to reduce or even avoid capital gains tax, including strategic selling, gifts, and offsetting previous losses. However, crypto income is always taxed in the year it is received.

Do You Have to Pay Tax on Crypto in the US?

In short, yes. Taxes apply when you sell, send, spend, or earn crypto if any of these activities result in a gain. Capital gains tax applies when you sell for a profit, and income tax applies to crypto earnings like staking or mining.

Cryptocurrencies like Bitcoin and Ethereum are unregulated financial instruments. However, the IRS treats digital assets as property, meaning they’re taxed like similar capital investments, such as stocks and mutual funds. Whether or not you’ll be required to pay tax depends on many different variables, including your income tax bracket in some cases. Nonetheless, there are two forms of IRS crypto tax that you need to be aware of: capital gains and income tax. Let’s discuss capital gains first.

Just like stocks, tax on crypto gains only applies to realized profits. In simple terms, this means that you’ve sold the cryptocurrencies for a profit. Suppose you bought 1 Bitcoin in January 2025 for $89,000. You sold your 1 Bitcoin in March 2025 when it was worth $90,000. Therefore, your realized capital gains are $1,000. In this instance, the crypto investment was held for under 12 months, so short-term capital gains tax rates apply. In most cases, short-term capital gains are taxed at your normal income tax rate.

Long-term rates apply if cryptocurrencies are held for over 12 months and are taxed at 0%, 15%, or 20%, depending on your income.

However, crypto users may also encounter a second tax liability due to crypto income, such as income staking and yield farming. Unlike capital gains, the IRS views crypto income the same as any other income stream – such as employment, stock dividends, or taxable bond interest payments. Therefore, crypto income is always taxed in the same year it was received. Keep in mind that if you’re mining or staking crypto as a business, you’ll be subject to self-employment tax (15.3%) in addition to income tax.

It’s important that you’re aware of how cryptocurrency taxes work – and you also need to know how to avoid them while following the tax rules. Seasoned investors use several strategies to reduce tax liabilities, which we’ll detail in this guide. Examples include crypto tax harvesting, taking advantage of long-term capital gains rates, gifting, and holding investments in Individual Retirement Accounts (IRAs).

At the same time, the IRS is clamping down on crypto tax evasion (which is different from tax avoidance), with U.S.-listed exchanges now reporting customer holdings. As such, this guide will prepare you accordingly.

Potential Upcoming Crypto Tax Changes in the US

As of Jan. 2025, centralized exchanges and brokers are required to report gross proceeds from crypto transactions on Form 1099‑DA to the IRS and the taxpayers. In 2026, Form 1099-DA will also include cost basis information. This enables the IRS to calculate capital gains more easily, as it will receive both proceeds and basis costs directly from crypto exchanges, thereby reducing the scope for tax errors.

The IRS also issued new guidance for tracking the cost base of cryptocurrencies (Revenue Procedure 2024-28). As of Jan. 2025, all taxpayers must switch to the per-wallet or per-account cost-tracking method. This could increase reported capital gains for many taxpayers in the US, as they won’t be allowed to pick the highest cost basis from one wallet to minimize gains when selling.

In Dec. 2025, US representatives Max Miller and Steven Horsford introduced a bipartisan draft bill called the Digital Asset PARITY Act to modernize the tax treatment of digital assets. The PARITY Act draft would exempt small stablecoin transactions (under $200) from capital gains taxes and allow stakers to defer taxation of staking and mining rewards for up to five years, instead of being taxed upon receipt. However, the PARITY Act is still considered a legislative draft, meaning it’s subject to significant changes.

How Is Cryptocurrency Taxed?

Decentralized finance (DeFi) and crypto lending represent some of the newer opportunities in the crypto space. Some types of crypto activities, such as DeFi yields, will trigger a tax obligation, while others (such as transfers between crypto wallets that you own) will not. The specific type of tax treatment and applicable rates will also vary depending on the type and duration of the event.

This section discusses the most common scenarios that crypto investors may face while reporting crypto taxes, and how the IRS taxes them. Notably, taxable events typically hinge on assets changing hands. Let’s look at some examples.

Profitable Crypto Investments

Most of you will be wondering about taxes on profitable crypto investments. If you’ve previously invested in stocks, the same rules apply to crypto assets. In a nutshell, the IRS looks at assets that have changed hands, creating a gain or a loss. They refer to these events as disposals.

- So, suppose you bought 1 Bitcoin in April 2020 when it was worth $5,000.

- You’re still holding today. Let’s say at current BTC/USD prices, your 1 Bitcoin is worth about $89,000

- This investment has produced gains of $84,000

Crucially, the Bitcoin has not been disposed of, meaning that your $84,000 profit is unrealized. The gain remains unrealized until you decide to sell. When you do, your profits are realized, meaning they are subject to capital gains tax.

In this example, you held the investment for over 12 months. So, regardless of when you decide to cash out, long-term capital gains tax rates will apply. Conversely, selling within 12 months of making the investment triggers short-term capital gains tax rates.

Now, here is some important information on what the IRS considers realized profits.

There is a misconception that capital gains are only realized when cryptocurrencies are sold for U.S. dollars (or another fiat currency). However, this simply isn’t the case.

Gains are realized as soon as the cryptocurrencies are disposed of, whether that’s for U.S. dollars or another digital asset. For instance, in the above example, you had $84,000 of unrealized profit. If you exchanged Bitcoin for Ethereum, capital gains tax would still be due on the $84,000 gain – even though it hasn’t been converted to “real money.”

Trading Cryptocurrencies

Things get really complicated when you actively trade new cryptocurrencies. As emphasized above, the IRS considers every trade a disposal. This means that each sale must be accounted for in terms of cost and disposal prices. This can be challenging when you’re regularly buying and selling different cryptocurrencies on various platforms.

Let’s look at an example to clear the mist:

- Let’s say you buy $5,000 worth of Ethereum, as you’re planning to trade on the best no-KYC crypto exchanges. When you make the purchase, Ethereum is worth $2,000. This is your cost price. The IRS refers to this as a cost basis.

- A few days later, you transfer Ethereum into Uniswap and exchange all of the tokens for Decentraland. At the time of the trade, Decentraland was worth $0.50.

- However, a few days have passed since you bought Ethereum. When you made the exchange for Decentraland, it was worth $2,200. You originally paid $2,000, so in the eyes of the IRS, you’ve made a capital gain of 10%.

- A few more weeks have passed, and you swap Decentraland back to Ethereum. When you trade, Decentraland is worth $1. This represents a capital gain of 100%, as you originally paid $0.50 per token.

In the above example, you bought Ethereum for cash, swapped the tokens for Decentraland, and then eventually went back to Ethereum. This triggered at least two realized capital gains because you sold the tokens for a higher price than you originally paid. Capital gains taxes apply even though crypto-to-crypto trades were involved.

Importantly, don’t think that you can evade paying taxes on crypto transfers just because you’re using a decentralized exchange. Although decentralized exchanges offer an anonymous user experience, blockchain transactions can still be tracked.

For instance, suppose you bought Ethereum (ETH) with a credit card on Coinbase and then transferred the Ethereum tokens from Coinbase to a decentralized exchange. Any future transactions that occur from the initial ETH holding can be traced back to your original purchase on Coinbase, which is associated with your identity.

Earning Crypto Income on DeFi Investments

Another misconception in the crypto space is that income from decentralized finance, such as staking, yield farming, or crypto savings accounts, isn’t taxed. Much like other yield income in traditional finance, these transactions are taxable. Staking rewards are taxable as ordinary income upon receipt, that is, when you gain “dominion and control” over them. Reporting crypto taxes from staking rewards requires listing them as “Other Income” on Form 1040, Schedule 1, Line 8z.

You must also report your capital gains and losses from selling staking rewards using Form 8949 and Schedule D. If you hold the tokens for one year or less, gains are taxed at short-term rates. If you hold them more than a year, gains are taxed at long-term rates.

Crypto income taxes are due in the same year they are received. This can be complicated, as crypto income should be reported based on its market price when received. For instance, some DeFi products distribute earnings weekly or even daily. This means you’ll have many different cost prices to calculate.

Let’s look at an example of how DeFi income is taxed:

- You invest 10 ETH into a DeFi platform, opting for a staking pool that pays 30% per year. If you keep your ETH in the pool for a year, you’ll earn 3 ETH in rewards (30% of 10 ETH). However, distributions are made weekly.

- After the first week, you receive your first distribution of 0.057 ETH. At the time, ETH is worth $2,000, so your rewards are worth approximately $114.

- In the second week, you receive another 0.057 ETH, but now ETH is priced at $2,500. Therefore, our reward from this week is worth $142.50.

- You must document these amounts as values in USD when receiving staking rewards each week.

In the example above, you received $114 and $142.50 worth of ETH rewards. These amounts must be reported as income to the IRS and are added to any other income you earn during the year.

For instance, if you earned $20,000 from a part-time job and $5,000 selling items on eBay, along with your staking rewards, your total income would be $25,256.50. This total income will be taxed according to your income bracket (more on this later).

Important: DeFi income can also trigger crypto capital gains tax. This will be the case if you sell your crypto income for a profit. The cost basis is determined by the price when you receive the income. Suppose you receive staking rewards of 1 ETH. At the time, Ethereum was worth $1,500. When you sell your 1 ETH reward, Ethereum is worth $1,700. Therefore, you’ve made capital gains of $200, even though you didn’t pay for the ETH.

Paying for Goods or Services With Crypto

There’s a lot of misinformation online about using crypto to pay for goods or services, and the tax implications that follow. As mentioned earlier, the IRS considers crypto profits as realized once the crypto is used, not just when sold or exchanged. In effect, crypto changing hands likely triggers a taxable event.

When you spend crypto, it triggers a taxable event based on the price when acquired versus when spent. Whether or not tax needs to be paid depends on the original and disposal prices.

For example:

- Suppose you buy 2 Bitcoins, each costing $15,000, and store them in a private wallet.

- After a few months, Bitcoin’s value rises to $20,000. You use 0.1 BTC to purchase an airline ticket.

- The IRS sees this transfer of 0.1 BTC to the airline as a disposal.

- At the time of disposal, Bitcoin’s value has increased by $5,000 per coin. Since you used 0.1 BTC, you realize a capital gain of $500 from this increase ($20,000 – $15,000 = $5,000 gain; $5,000 x 0.1 = $500).

- This $500 will be added to your capital gains liability for the tax year.

It’s important to keep detailed records of all crypto transactions for accurate tax reporting.

Crypto Mining

Crypto mining rewards are also taxable. Just like DeFi rewards, such as staking or yield farming, crypto mining is considered income. Mining rewards from mining cryptocurrency are taxed as ordinary income. The tax is based on the value of the coins at the time you receive them.

For example, imagine that in the first week, you mine 1 BTC, which is worth $40,000. You must report this $40,000 as part of your income for the year. Remember, this doesn’t mean you’ve made $40,000 clear because mining often has high costs. Mining or staking crypto as a business is subject to ordinary income tax and a self-employment tax (15.3%). These earnings must be reported on a Schedule C (Form 1040).

If you’re a registered mining company, you’ll be able to offset the expenses required for mining. This primarily includes energy costs and hardware maintenance. Additionally, selling the 1 BTC mined could trigger capital gains tax. Similar to DeFi income, this tax is based on the price at which the mining rewards are sold.

For example, if you sold the 1 BTC when it was worth $50,000, you would have made a capital gain of $10,000. This is because you initially received the 1 BTC when it was valued at $40,000.

Selling Goods for Crypto

We mentioned earlier in our crypto taxes USA guide that buying goods with crypto can trigger a taxable event. But what about selling goods for crypto? The same rules apply, but in reverse.

- For example, suppose you sell your car for $20,000. You originally paid $30,000, so there are no capital gains on the sale.

- The buyer pays you in Bitcoin, which is currently worth $40,000. Therefore, you receive 0.5 BTC from the buyer.

- You hold onto the 0.5 BTC for a few more months.

- When you’re ready to sell, Bitcoin is valued at $80,000. As such, you sell your 0.5 BTC for $40,000, making a $20,000 profit.

- The realized capital gain is $20,000, which will be taxed accordingly.

Note that if you had sold the car for more than you originally paid, capital gains tax on the sale would also apply.

Unprofitable Crypto Investments

Although we often focus on profitable crypto investments, not all investments yield a profit. What happens when you make a loss? Fortunately, the IRS has very favorable rules on capital losses, which also apply to cryptocurrency investments.

Simply put, if you dispose of a cryptocurrency at a loss, you can use these losses to offset your capital gains liability.

Let’s look at a hypothetical example of how this works in practice:

- You buy 10,000 DOGE tokens when Dogecoin is worth $1. This takes your total investment to $10,000.

- A few months later, you sell your 10,000 DOGE tokens. At the time of the sale, Dogecoin is worth just $0.30. This means you receive $3,000 back, even though you originally invested $10,000.

- On this investment, you lost $7,000.

- Without this loss, your total capital gains for the year were $9,000. You can now deduct the $7,000 Dogecoin loss from this gain. Your capital gains for the year become $2,000.

Some investors strategically sell their cryptocurrencies at a loss. This helps them reduce their tax bill for the year. This is known as tax-loss harvesting, and it’s one of the best ways to avoid crypto taxes.

It’s also important to note that if your capital losses exceed your gains, you can deduct up to $3,000 of these losses against your ordinary income each year. Any remaining losses can be carried over into future years indefinitely. As such, learning how to claim crypto losses on taxes can be helpful in 2026.

In the example above, you made $7,000 in capital losses from the Dogecoin investment. Suppose you made just $2,000 in capital gains in the same year. You would use $2,000 from your Dogecoin losses to bring the capital gains to $0. In the following year, you could use the remaining $5,000.

Receiving a Salary in Crypto

According to a CNBC report, more than half of Americans aged 25 or under would be happy to receive their salary in crypto. From a tax perspective, the rules are much the same as receiving your salary in dollars.

However, it’s important to remember that your income is based on the value of the crypto when it’s received. For example, suppose your monthly salary is 0.1 BTC. When paid, Bitcoin is worth $30,000. Therefore, you received 0.1 BTC, making your income $3,000 for that month. This amount needs to be added to your income for the tax year.

Additionally, don’t forget about disposals. At some point, whether through cashing out or spending the crypto, it will be sold. If this disposal results in a profit, capital gains tax will apply.

For instance, if you sell your monthly salary of 0.1 BTC when Bitcoin is worth $40,000, and you originally received it at $30,000, this would represent a capital gain of $1,000 ($40,000 – $30,000 = $10,000; $10,000 * 0.1 BTC = $1,000).

Donating Crypto

The IRS views cash and crypto donations similarly. This means that crypto donations can help you offset your tax liability. However, it’s important to consider the cost basis and the fair market value at the time of the transaction.

For example, let’s say you bought 1 Bitcoin in 2022 for $16,000. By 2026, that Bitcoin is worth $89,000. This increase would represent a capital gain of $73,000 if you were to sell it. However, if you donate the Bitcoin to charity, you could potentially offset $89,000 from your taxable income. This is because the deduction is based on the market value at the time of the donation.

There are specific rules to be aware of before donating crypto for tax advantages. For instance, the maximum you can deduct for non-cash assets like crypto is 30% of your adjusted gross income (AGI). Anything exceeding this limit can be carried over into future tax years. Additionally, for donations exceeding $5,000 in value, you must obtain a qualified appraisal to substantiate the claimed value of the cryptocurrency.

Gifting Crypto

Similar to donating crypto, gifting is another common way for investors to reduce their tax burden. There are two angles to consider: the person giving the crypto gift, and those receiving it.

The Giver

- Suppose an investor buys 1 BTC at $15,000.

- Two years later, Bitcoin is worth $25,000. If sold, this would trigger a capital gain of $10,000.

- However, the investor decides to gift 0.5 BTC. The other 0.5 BTC remains in the investor’s private wallet.

- The 0.5 BTC gift does not trigger a taxable event if its value is below the annual gift tax exclusion limit.

The Receiver

- The person receiving the crypto gift receives 0.5 BTC.

- When the gift was received, Bitcoin was valued at $25,000. This means the receiver has $12,500 worth of Bitcoin.

- However, the receiver acquires the original cost basis that the investor paid, which was $15,000 for the 1 Bitcoin.

- So, for the 0.5 BTC gift, the receiver’s basis is $7,500.

- If the receiver sells the 0.5 BTC for $10,000, the capital gains on the sale would be $2,500 ($10,000 – $7,500), which the receiver must report and pay tax on, depending on whether the holding period qualifies for short- or long-term capital gains.

In 2026, you can gift up to $19,000 without reporting the transaction to the IRS. Anything above this needed to be reported. If the gift exceeds this amount, the giver will need to report it using IRS Form 709, but no taxes are owed unless they exceed the lifetime gift limit ($15 million in 2026).

Trading Stablecoins

Stablecoins track the value of a target asset, such as the USD. The most popular stablecoins (USDT and USDC) are both backed by US dollar-based assets. Buying stablecoins with USD is unlikely to create a meaningful tax burden because these tokens generally maintain parity with the USD. However, they can depeg from the dollar, which could lead to a taxable event if you exchange these tokens when their price diverges from $1.00. Like any crypto trade, keep stablecoin purchases and sales records for tax-reporting purposes.

Exchanging more volatile cryptocurrencies with stablecoins can create a tax liability similar to trading with USD. However, record-keeping requires an extra step, as you must account for any variance between the value of the stablecoin and the USD. While generally equivalent to a pegged asset, such as USD, stablecoins can fluctuate in value.

Trading NFTs

Non-fungible tokens (NFTs) are unique assets on the blockchain, typically representing ownership or rights. Most commonly, we see these as digital art, with some NFT collections routinely trading for four or five figures. Generally speaking, NFT trades follow similar tax rules to other cryptocurrencies, with short-term capital gains applying to assets held less than a year. When sold, NFTs held for more than a year enjoy lower long-term capital tax rates.

However, NFTs deemed collectibles are subject to a higher tax rate of 28%, whereas other capital gains fall into 0%, 15%, or 20% brackets for most traders based on taxable income.

The basic groupings for NFT taxes follow as outlined below:

- Non-collectible NFTs: Taxed in accordance with standard short or long-term capital gains tax rates.

- Collectible NFTs: Taxed as collectibles and subject to 28% taxes. Short and long-term rates do not apply.

- Creator Sales: Initial sales of NFTs are taxed as ordinary income for the creator. Businesses may be able to deduct associated expenses on Schedule C.

- Royalties: NFT royalties based on aftermarket sales or other permitted uses are taxed as ordinary income for the person or company receiving royalties.

- NFT Staking: Some platforms support NFT staking, which allows for the possibility of earning additional cryptocurrencies. These earnings count as ordinary income and must be reported using their USD value at the time they are received.

As with other cryptocurrencies, NFT transactions must be reported to the IRS using their value in dollars at the time of the transaction.

Airdrops, Hard Forks, and Token Rewards From DAOs

Airdrops, hard forks, and other “free” tokens count as gross income in the year they are received. Their USD values at the time of the transaction must be reported to the IRS and become part of your taxable income. Values at the time of receipt become your cost basis for the purposes of calculating short or long-term capital gains if you later sell, exchange, or spend the tokens.

Crypto as Part of an Inheritance

The IRS views crypto as property rather than as a currency. As such, crypto passed on as part of an inheritance or an estate follows the same rules and exemptions as other types of property. Crypto passed on as part of an inheritance is exempt from estate taxes if the estate’s total value is less than the federal exemption limit ($15,000,000 per person in 2026).

However, each of the 50 states has its own laws regarding inheritance. While most people will not be liable for federal estate tax, state laws can create a tax bill.

The inheritor also inherits the cost basis as the USD value at the time of inheritance. A wiser way to pass on cryptocurrency may be to gift the crypto to your intended recipient before passing. In many cases, this strategy reduces the recipient’s cost basis, thereby reducing the future tax liability upon disposition (sales or use).

How Much Are Crypto Taxes in the U.S.?

In short: Crypto held for less than 12 months is taxed as short-term capital gains at rates up to 37%. If you hold for more than 12 months, long-term capital gains rates (0%, 15%, or 20%) apply.

Unless you’re heavily invested in DeFi earning tools like staking or yield farming, your main tax liability will likely come from capital gains. In general, the amount you pay depends on two key factors:

- How much profit you made from the cryptocurrency investment.

- How long you’ve held the cryptocurrency investment before selling.

First, the profit is simply the sale price minus the original cost. For example, you buy ETH for a total outlay of $10,000. Later, you sell the entire ETH investment for $15,000, meaning your capital gains are $5,000. Notably, trading costs affect your cost basis, similar to how they apply to stocks’ cost basis. Your cost to acquire virtual assets is added to the cost basis of those assets for tax calculations. However, let’s look at the simple math, assuming trading costs are negligible.

The amount of taxes you need to pay on the $5,000 gain depends on whether you held the investment for more or less than 12 months.

- Let’s say you bought the 10 ETH in January, and sold the tokens in October of the same year.

- Since this is less than 12 months, short-term capital gains tax applies.

- In this case, your $5,000 gain is added to your total income for the year.

- If you earned a salary of $50,000, your total income is $55,000, and it will be taxed accordingly.

That said, different rules apply for certain situations – such as filing jointly as a married couple. The section below provides a breakdown of what to expect.

So, what about selling crypto after holding it for at least 12 months? In this case, long-term capital gains tax rates apply. These offer more favorable rates, as U.S. investors are encouraged to hold long-term.

There are three potential long-term capital gains tax rates: 0%, 15%, and 20%. The rate is based on your total taxable income for the year, which includes capital gains. For instance, suppose you earn a salary of $30,000 and make $5,000 in long-term crypto gains. This would bring your total taxable income to $35,000.

Crypto Tax Rates

We’ve clarified that the duration you hold your crypto investment — less than 12 months for short-term and over 12 months for long-term — affects the tax rates. To help you determine your crypto taxes in 2025 and 2026, we’ve created the tables below. Please refer to the short-term crypto tax rate table below for investments held for less than 12 months. According to federal income tax brackets, short-term capital gains are taxed at ordinary income tax rates. These tax brackets adjust annually for inflation.

2026 Income Tax Brackets

The table below details the 2026 tax brackets that apply to income for US taxpayers. Crypto income, such as staking rewards or DeFi yields, is added to regular income and any 1099 income for tax purposes. Additionally, these rates apply to short-term gains for assets held for less than a year.

| Tax Rate | Single | Head of Household | Married Filing Jointly | Married Filing Separately |

| 10% | $0 to $12,400 | $0 to $17,700 | $0 to $24,800 | $0 to $12,400 |

| 12% | $12,401 to $50,400 | $17,701 to $67,450 | $24,801 to $100,800 | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 | $67,451 to $105,700 | $100,801 to $211,400 | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 | $105,701 to $201,775 | $211,401 to $403,550 | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 | $201,776 to $256,200 | $403,551 to $512,450 | $201,776 to $256,225 |

| 35% | $256,226 to $640,600 | $256,201 to $640,600 | $512,451 to $768,700 | $256,226 to $384,350 |

| 37% | $640,601 or more | $640,601 or more | $768,701 or more | $384,351 or more |

2026 Long-Term Capital Gains Rates

If you held the investment for 12 months or more, refer to the long-term crypto tax rates below. Long-term capital gains tax rates vary based on income and filing status.

| Tax Rate | Single | Head of Household | Married Filing Jointly | Married Filing Separately |

| 0% | Less than or equal to $49,450 | Less than or equal to $66,200 | Less than or equal to $98,900 | Less than or equal to $49,450 |

| 15% | $49,451 through $545,500 | $66,201 through $579,600 | $98,901 through $613,700 | $49,451 through $306,850 |

| 20% | Over $545,500 | Over $579,600 | Over $613,700 | Over $306,850 |

You pay taxes on your income based on different rates, grouped into what are called tax brackets. As your income increases, the amount of tax you pay on new earnings rises, moving you into a higher bracket. However, this higher rate only applies to the portion of your income that falls within that new bracket – not your entire income.

Notably, most US filers also qualify for deductions or exemptions that lower their taxable income. The IRS released tax inflation adjustments for tax year 2026, which states that a single filer can claim a standard deduction of $16,100, reducing the income subject to federal income tax by that amount. Married couples may claim $32,200 for the 2026 tax year. Optionally, households can opt for itemized deductions. However, the standard deduction typically results in lower taxes for most households.

Are There Any Tax-Free Crypto Transactions?

In short: There are no taxes on crypto transactions that involve buying crypto with fiat, transferring coins between your wallets, gifting under $19,000 (in 2026), and donating to charity.

Fortunately, not all crypto transactions trigger a taxable event.

Here are some examples of tax-free transactions available to U.S. residents:

- Buying Crypto With Fiat: No tax is due when purchasing crypto with fiat money. This is similar to buying stocks, ETFs, or any other investment asset.

- Transferring Crypto Between Your Own Wallets: You can freely transfer crypto between your own wallets without triggering a tax event. For instance, moving Ethereum from MetaMask to Trust Wallet, or Bitcoin from Electrum to Coinomi. Additionally, you can transfer crypto from a private wallet to an exchange without the transaction being taxed. However, once you dispose of the crypto (either for fiat or another crypto), this will trigger a tax event.

- Gifting Crypto: In 2026, you can gift up to $19,000 worth of crypto without triggering a tax event. While you can gift more than this without paying tax, amounts above $19,000 need to be reported to the IRS.

- Donating Crypto: You can donate crypto to a registered charity without being taxed. However, due to new IRS Revenue Procedure 2024-28, as of Jan. 2025, you must switch to wallet-based tracking. I.e., instead of universally tracking all assets across all accounts, you must now track and report digital asset transactions separately for each wallet and account.

- Holding Crypto: In the U.S., only realized capital gains trigger a tax event, meaning tax is due when the crypto is actually disposed of by selling or spending it. This means you can hold crypto in your wallet for as long as you want without needing to worry about taxes.

How to Calculate Crypto Tax

In short: Subtract what you paid for the crypto from the price at the time of disposal. Your tax rate depends on how long you’ve held it, your income for the year, and your filing status.

We briefly covered some examples of how to calculate crypto taxes, including capital gains and income. Let’s look at some more detailed examples.

Calculating Short-Term Crypto Gains

- In January 2026, you buy $10,000 worth of Bitcoin. Later in the year, you sell the entire position for $20,000. Your short-term capital gain on this trade is $10,000. Your trading costs for the trade were $100. This increases your cost basis, ultimately reducing your taxable income from the trade due to the adjustment. Your taxable income in this example equals $9,900.

- In 2024, you also earned a salary of $60,000. Adding your short-term capital gains of $9,900 brings your total income for 2024 to $69,900.

Note: The following calculations assume a single filer using the standard deduction ($16,100 for 2026). For simplicity, they also ignore other possible income-based taxes that may apply, such as FICA taxes, self-employment taxes, or state taxes.

Since these assets were sold in 2025, you calculate your taxes using the 2026 tax rates. First, let’s take the standard deduction of $16,100.

$69,900 – $16,100 = $53,800.

Now, let’s see how much is due in taxes:

- You’ll pay 10% on the first $12,400 income, which equals $1,240.

- You’ll pay 12% on income between $12,401 and $50,400. That’s $37,999 taxed at 12%, totaling $4,559.

- The remaining $3,400 of your income ($53,800 – $50,400) is taxed at 22%, which comes to $748.

In total, your tax for the year is $6,547 ($1,240 + $4,559 + $748)

Calculating Long-Term Crypto Gains

Now, let’s look at how to calculate long-term capital gains. We’ll use the same figures to show how long-term holders benefit from more favorable tax rates.

To recap, you bought $10,000 worth of BTC and sold it for $20,000, for a total capital gain of $10,000. However, you held for over 12 months in this example, so long-term capital gains rates apply. Your salary and other ordinary income are taxed at your normal tax rate. The $10,000 profit becomes a separate calculation because you qualify for long-term capital gains.

As before, we have to consider taxable income, which is your income ($60,000) minus either the standard deduction or allowable itemized deductions. We’ll use the standard deduction for a single filer ($16,100). This reduces your taxable income to $43,900.

In 2026, single filers pay 0% long-term capital gains taxes if their taxable income is less than $49,450 . In this example, there is no capital gains tax due. If the taxable income was between $49,451 and $545,500, however, the long-term capital gains tax on the $10,000 gain jumps to 15%.

The rest of the tax calculation relies on taxable income from all other sources, which in this case is $60,000 minus the standard deduction of $16,100. We’ll also ignore the $100 trading fees because they don’t affect the calculations below.

- You’ll pay 10% on the first $12,400 income, which equals $1,240.

- You’ll pay 12% on income between $12,401 and $50,400. That’s $37,999 taxed at 12%, totaling $4,559.

Only $49,450 is taxable as regular income. Holding for the long-term gains rate removed the $10,000 profit from the total income subject to regular income tax.

In total, your tax for the year is $5,799 ($1,240 + $4,559). However, with a slightly higher income, the trade would have fallen into the 15% bracket, adding $1,500 to the tax bill for long-term capital gains.

By contrast, the same profit and income with a short-term gains tax rate cost $7,219 in taxes. In effect, taking short-term profits in the earlier example pushed some of the “income” from the trade into a third tax bracket taxed at 22%. In many cases, simply holding for at least one year can result in substantial savings ($2,615 in this example).

Calculating Crypto Income

Now that we’ve explained how to calculate capital gains taxes, let’s move on to crypto-related income. Generally, most income sources—whether from staking, yield farming, or mining—follow the same tax rules.

- In this example, we’ll consider an investor who buys Bitcoin with a credit card, for a total of $20,000. At the time, Bitcoin is worth $20,000, so the investor receives 1 BTC.

- They instantly deposit the 1 BTC into a savings account that offers a 5% annual yield. At this point, no taxable event has occurred.

- The Bitcoin savings account pays out quarterly. Over the course of a year, 5% of 1 BTC earns 0.05 BTC in rewards. Split across four quarters, this results in four distributions of 0.0125 BTC each.

Naturally, on each quarterly payment, the value of Bitcoin will be different.

| Bitcoin Price | Quarterly Rewards | Value of Rewards in USD | |

| Payment 1 | $25,000 | 0.0125 BTC | $313 |

| Payment 2 | $30,000 | 0.0125 BTC | $375 |

| Payment 3 | $21,000 | 0.0125 BTC | $263 |

| Payment 4 | $40,000 | 0.0125 BTC | $500 |

| Total | 0.05 BTC | $1,450 |

So, the table above shows the value of each quarterly distribution in dollars. Added together, the total income generated from the Bitcoin savings account was $1,450.

This amount simply needs to be added to the total income for the year. For instance, if the investor’s taxable income was $50,000, their total income for the year would be $51,450. This amount will be taxed according to the progressive tax system discussed earlier.

However, this assumes that the Bitcoin rewards were not sold. If they were sold, it would trigger a taxable event, as the Bitcoin would be considered disposed of. For example, if the investor received their first distribution when Bitcoin was valued at $25,000 and instantly sold it at the same price, there would be no capital gains because the cost basis and sale price are the same.

Conversely, if the investor held onto the rewards for a few more weeks, the situation would change. Initially, the 0.0125 BTC reward was worth $313. But if the investor sells it later for $333, they would have a capital gain of $20. This would need to be added to any other short-term capital gains for the tax year.

That said, if the investor sold their Bitcoin rewards for a lower price than when they were originally received, a capital loss would occur. As noted, this can be offset against capital gains liabilities for the year.

Additionally, the investor must also consider the tax implications once the 12-month savings period ends.

This is because the investor will receive their original 1 BTC back from the savings account. When it was originally deposited, the 1 BTC was worth $20,000. After 12 months, it is worth $40,000. Therefore, the investor has made long-term capital gains of $20,000.

Crucially, the capital gain is only realized if the investor sells the 1 BTC. If they choose not to sell, no tax is due since the asset hasn’t been disposed of.

Calculating Cost Basis

Cost basis is the original price you paid for a cryptocurrency, plus fees. For example, if you buy BTC for $1,000 and pay a $10 transaction fee, your cost basis is $1,010. When you sell cryptocurrencies, you subtract the cost basis from the sale price to calculate your capital gain/loss. For example, if you buy BTC for $1,000 and sell it for $2,000, you have a $1,000 gain. On the other hand, if you sell it for $500, you have a $500 loss.

However, if you sell the same cryptocurrency multiple times at different prices, you must use cost basis methods like FIFO, LIFO, or HIFO to determine in which order your cryptocurrency gets disposed of.

- FIFO (first-in first-out: The first cryptocurrency you purchased is the first you dispose of.

- LIFO (last-in first-out): The last cryptocurrency you acquired is the first you dispose of.

- HIFO (highest-in first-out): The highest price cryptocurrency you acquire is the first you dispose of.

For example, you buy BTC in Jan. for $10,000, in Feb. for $40,000, and in March for $30,000, and sell it in April for $45,000. In this case, the cost basis and the capital gain will be as follows:

| Method | Sell Order | Cost Basis | Calculation | Capital Gain |

| FIFO | January | $10,000 | $45,000 – $10,000 | $35,000 |

| LIFO | March | $30,000 | $45,000 – $30,000 | $15,000 |

| HIFO | February | $40,000 | $45,000 – $40,000 | $5,000 |

Which method to use? The answer will depend on your goal. On that note, use HIFO to lower your taxable capital gain, FIFO to reduce capital gains during bear markets, and LIFO to reduce short-term taxable gains during bull markets.

Revenue Procedure 2024-28

In 2024, the IRS issued Revenue Procedure 2024-28 to provide taxpayers with a safe harbor. Revenue Procedure 2024-28 ended the “universal” cost base method for digital assets by introducing new rules for tracking the cost base of cryptocurrencies. Each wallet or account is now treated as an independent ledger. From Jan. 1, 2025, all taxpayers must switch to the per-wallet or per-account cost-tracking method – you must track and report your crypto transactions separately for each wallet and account.

Before the IRS issued Revenue Procedure 2024-28, you could buy cryptocurrencies on Binance, transfer them to Best Wallet, and sell them on OKX since all transactions for a specific coin were combined into a single queue, regardless of where they were held. Under the new rules, each wallet or account must hold its separate cost basis records.

For example:

- You use MetaMask to buy 1 BTC at a cost basis of $20,000.

- You use Best Wallet to buy 1 BTC at a cost basis of $40,000.

- Later, you sell 1 BTC from Best Wallet for $60,000.

Since the sale comes from Best Wallet, you must use the cost base of that specific wallet to calculate your gains/losses ($60,000 – $40,000). You cannot use the lower cost basis from MetaMask to reduce your taxable gain. In this example, you pay tax on a $20,000 gain.

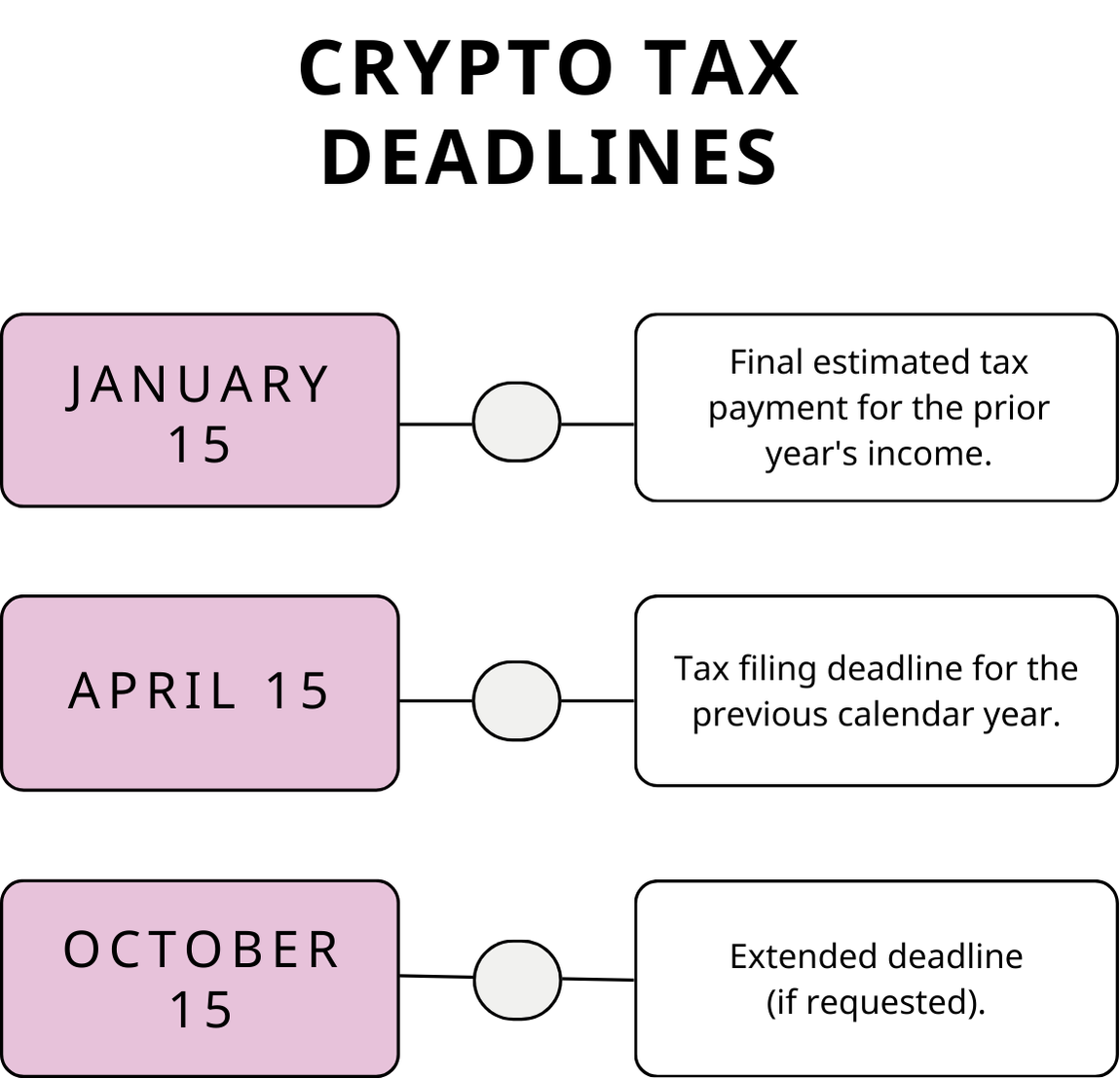

When Do You Have to Pay Crypto Taxes?

In general, any capital gains or income made from crypto needs to be paid the following year. For example, crypto taxes from 2025 must be reported in 2026. More specifically, “tax season” runs between January 1st and April 15th each year, meaning you’ll need to pay within this time frame. This is why it’s crucial to get your crypto taxes in order. For the 2025 tax year, the deadline to file your federal income tax return is April 15, 2026.

- April 15: Deadline to file your crypto tax return and pay taxes for the previous calendar year (January to December). This includes taxes on crypto gains, income, and other sources from the prior year.

- October 15: Extended deadline to file your tax return if you requested an extension. This is still for taxes owed from the previous calendar year, but any unpaid taxes should have been settled by April 15.

- January 15: Deadline for the last estimated tax payment. This covers income from September to December of the previous calendar year.

Leaving things to the last minute can result in delays, meaning potential fines from the IRS. Keep thorough records as you go. If you’re an active trader, it’s a good idea to use a crypto tax software provider. Examples include Koinly, CoinTracker, and CoinLedger, among others.

How to Report Cryptocurrency Tax

In short: Report capital gains and losses on IRS Form 8949, and summarize them on Schedule D of Form 1040. Crypto income should be reported on Form 1040, Schedule 1. Beginning Jan. 1, 2025, centralized exchanges and brokers must report the gross proceeds from crypto sales and exchanges on a new tax form – 1099-DA. For example, if you sold Ethereum for $3,000, this will be your gross proceeds, even if you initially paid $2,000. Beginning Jan. 2026, brokers will also need to report the cost basis – original purchase price plus fees.

Once you’ve calculated your crypto taxes for the year, the next step is filing them with the IRS. The process generally involves the following forms:

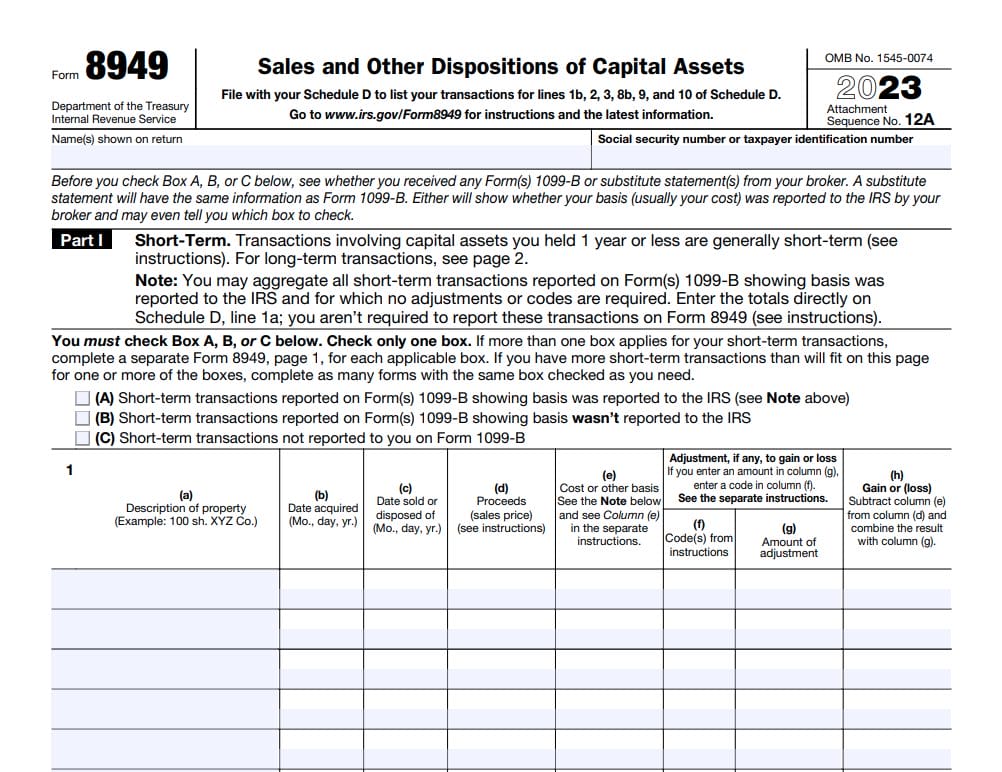

IRS Form 8949

First, you’ll need to complete IRS Form 8949. This tax form is used to report any capital gains or losses for the year. For each transaction, you’ll need to fill out the date you bought and sold the cryptocurrency, alongside the respective cost and sale prices.

This form is only for capital gains; we’ll come to crypto income shortly. Moreover, you should also add any other capital disposals made for the year, such as stocks, ETFs, or property.

Schedule D on IRS Form 1040

Now that you’ve totaled all your capital gains and losses for the year, you must transfer the totals to Schedule D on IRS Form 1040.

Add Crypto Income to IRS Form 1040

Now that you’ve covered capital gains, let’s move on to crypto income. This must also be added to Form 1040, but in Schedule 1 under ‘Additional Income and Adjustments to Income.’

Submit to the IRS

Once you’ve completed IRS Form 8949 and 1040, you can submit them to the IRS. Use the data from the Form 1099-DA to complete your Form 8949 and Schedule D. Just make sure this is done before tax season closes on April 15th.

Many investors will use a qualified tax advisor who has experience in crypto assets. They will calculate all of your taxes on your behalf, fill out the required tax forms, and submit them to the IRS.

Does the IRS Track Crypto?

In short: Yes, the IRS can track crypto transactions, especially through U.S.-regulated exchanges. Make sure to report all crypto activities to avoid penalties.

As explained by CNBC, the IRS has many ways to track cryptocurrency investments made by U.S. residents. The best crypto exchanges in the U.S., such as Coinbase, Gemini, and Kraken, are legally required to submit customer transactions to the IRS.

Therefore, if the IRS opens an investigation into your trading activities, you’ll want to ensure you’ve already submitted the correct tax reports. Serious penalties could apply if taxes have been understated or not reported at all. Moreover, the IRS has other ways to track your cryptocurrency transactions, even if you’ve withdrawn to a private wallet.

- For example, suppose you originally bought $10,000 worth of Ethereum on Coinbase. As a regulated U.S. exchange, Coinbase conducts KYC (Know Your Customer) checks on all registered users.

- Therefore, you would have had to provide Coinbase with your personal information and government-issued ID before making the purchase.

- Next, you withdraw your Ethereum to a decentralized wallet like MetaMask. You use MetaMask anonymously and connect it to a decentralized exchange like Uniswap, where you swap Ethereum for Sandbox tokens.

- At this stage, although you’re trading anonymously, your original Ethereum purchase is still linked to your Coinbase account. Blockchain transactions are transparent, meaning all subsequent transactions can be tracked.

Ultimately, we strongly advise that you accurately report all cryptocurrency activities to the IRS. If you’re ever unsure about what needs to be reported, consult a qualified tax advisor.

Penalties for Tax Evasion

While we discuss legal ways to reduce crypto taxes in later sections, not reporting crypto gains or income is not among them. The IRS views crypto as property, so gains or income from crypto fall under the same tax reporting rules as similar property types. In 2021, the IRS began to pursue crypto tax evaders in earnest with “Operation Hidden Treasure,” designed to target virtual currency noncompliance. The still-ongoing effort attempts to connect pseudonymous crypto wallets with real-world people or entities that may not have paid taxes associated with the wallet transactions.

The consequences of finding yourself on the wrong end of an IRS judgment and prosecution can be dire. Civil and criminal penalties can reach up to $100,000 and up to five years in jail for failure to report or misreporting crypto income and gains. In 2022, the IRS announced the conviction of a Florida resident for attempted tax evasion on more than $1 million earned through crypto transactions. According to reports, despite using sophisticated techniques to conceal the money trail, the government was able to identify the person, who faces up to five years in prison.

Are There Ways to Reduce How Much Crypto Tax You Pay?

In short: You can reduce taxes by using strategies like tax-loss harvesting, gifting, or holding for more than 12 months to qualify for lower capital gains rates.

Now that we’ve covered everything there is to know about crypto trader tax in the US, we can now discuss some tax avoidance strategies. Read on to discover legal ways to reduce your taxes on crypto.

Tax-Loss Harvesting

In simple terms, tax-loss harvesting involves intentionally selling a cryptocurrency investment at a loss. This is done to gain tax advantages, as the loss can be offset against capital gains for the year.

For example:

- As the end of the year approaches, you’ve accumulated $20,000 in capital gains.

- Let’s say that you’re still holding 1 BTC in your crypto wallet, which you purchased for $50,000.

- Right now, Bitcoin is trading at $40,000, meaning you’re down $10,000.

- If you sell your 1 BTC, you can offset part of the $10,000 loss against your $20,000 capital gains.

- Only $3,000 can be offset each year against ordinary income, but any remaining losses can be carried over to future years.

Now, you may not have wanted to sell your Bitcoin – but you could do it in order to reduce your tax liabilities. You could also repurchase Bitcoin afterward, to ensure you continue holding it. This strategy of selling and repurchasing is not allowed in traditional investments due to the “wash sale” rule, which requires investors to wait 30 days before buying the same asset.

Keep in mind that the wash sale rule currently applies only to stocks, bonds, mutual funds, and ETFs, but not to crypto assets. This presents a unique tax-loss harvesting opportunity to pay less tax. For example, you can sell crypto at a loss, claim the deduction, and immediately buy it back, without having to wait 30 days.

Let’s say you buy Bitcoin for $90,000 and sell it for $80,000 to realize a $10,000 capital loss. If you repurchase BTC again at $80,000, this transaction won’t trigger a wash sale. You can use the $10,000 loss to reduce your capital gains tax. If your capital losses exceed your gains, you can deduct up to $3,000. However, this doesn’t apply to crypto ETFs as they are classified as securities, meaning they are subject to the 30-day wash sale rule. If you’re an active trader holding many different cryptocurrencies, it can be difficult to know which investments to sell to benefit from tax-loss harvesting. In this case, using crypto tax software is the way to go.

However, because the IRS treats Bitcoin as property and not a security like stocks and bonds, the wash sale rule doesn’t apply to cryptocurrency. If you’re an active trader holding many different cryptocurrencies, it can be difficult to know which investments to sell to benefit from tax-loss harvesting. In this case, using crypto tax software is the way to go.

Hold Your Crypto for at Least 12 Months

Another way to reduce your crypto taxes is to avoid selling for at least 12 months. In doing so, you’ll benefit from long-term capital gains rates. These are a lot more favorable than short-term capital gains, as we identified earlier.

For example, suppose you originally bought 5 BTC at $10,000 each, totaling $50,000. Each BTC is now worth $50,000, so your portfolio is valued at $250,000. If you sell today, that’s capital gains of $200,000. Selling within the 12-month period could mean paying a tax rate as high as 37%. Holding for at least 12 months means the most you can pay is 20%.

You should consider the risks of holding onto a profitable investment just to save tax. The crypto markets can be extremely volatile. Waiting for 12 months could mean losing all of the gains you’ve secured.

Gifting Crypto to Somebody on a Low Tax Bracket

Another strategy is to gift cryptocurrencies to someone in a lower tax bracket.

Here’s how it works:

- Let’s say you own 1 BTC, for which you originally paid just $2,000. Bitcoin is now worth $50,000, so your capital gains would be $48,000 if you cashed out.

- This could mean a huge tax bill as you’re in a high-income bracket. As such, you decide to gift the 1 BTC to a family member who is a low-income earner.

- Once you’ve made the transfer, you no longer own the Bitcoin, meaning you’re not required to pay tax.

The person who received the 1 BTC will inherit your original cost price, which was $2,000. If they sell it, they will have triggered capital gains of $48,000. However, as they’re in a low-income bracket, they pay significantly less tax.

Do note that the rules around gifting are very clear. The person receiving the crypto is the rightful owner. If they transfer the proceeds to you, they would be breaking the law. Additionally, we mentioned earlier that gifts of over $18,000 in 2024 need to be reported to the IRS. That said, this doesn’t mean that you’ll need to pay tax.

Donating Crypto to a Registered Charity

You might also consider donating crypto to a charity, which is another way to reduce or eliminate taxes. The donation can then be used to offset your taxable income. This is based on the market price at the time of the transfer.

Suppose you bought 3 ETH when they were worth $500 each. Let’s say ETH is now worth $1,500, so your investment is valued at $4,500. If you donate the 3 ETH tokens to a registered charity, you can offset the $4,500 donation as tax-deductible.

Conclusion

In summary, crypto taxes in the U.S. can no longer be ignored. Whether you’ve made capital gains or income, it’s likely you’ll need to submit a tax report to the IRS. That said, there are several legal tax avoidance strategies to consider before proceeding, such as tax-loss harvesting and ensuring you hold at least 12 months.

Overall, the best practice is to speak with a qualified tax advisor who has experience with crypto assets. Not only will they ensure you file your taxes correctly, but they might be able to help you reduce them.

FAQs

Do you have to pay tax on Bitcoin?

How much tax do you pay on crypto?

Do you have to report crypto under $600?

Do I need to report crypto if I didn’t sell?

References

- Frequently Asked Questions on Virtual Currency Transactions (IRS)

- Crypto Exchanges to Report Customer Data Under Treasury Proposal (Bloomberg)

- Bitcoin Quote (CNBC)

- Topic No. 409 Capital Gains and Losses (IRS)

- Want to Be Paid in Bitcoin or Dogecoin? Here Are the Rewards and Risks (CNBC)

- Charitable Deductions: Donating Cryptocurrency and NFTs for Tax Purposes (Reuters)

- Frequently Asked Questions on Gift Taxes (IRS)

- What Cryptocurrency Investors Should Know About Filing Taxes (CNBC)

- IRS releases tax inflation adjustments for tax year 2026 (IRS)

- 2026 tax brackets (Tax Foundation)

- Understanding your Form 1099-DA (IRS)

- Operation Hidden Treasure: The IRS vs. Crypto (Wealth Management)

2M+

250+

8

70

About Cryptonews

Our goal is to offer a comprehensive and objective perspective on the cryptocurrency market, enabling our readers to make informed decisions in this ever-changing landscape.

Our editorial team of more than 70 crypto professionals works to maintain the highest standards of journalism and ethics. We follow strict editorial guidelines to ensure the integrity and credibility of our content.

Whether you’re looking for breaking news, expert opinions, or market insights, Cryptonews has been your go-to destination for everything cryptocurrency since 2017.