Whales Moving Millions in Bitcoin as Hong Kong Regulator Makes Move

The world of crypto has received an unwelcome jolt after the Hong Kong financial securities regulator announced – somewhat abruptly – that all crypto exchanges will need to register with the body if they wish to continue trading.

Per Reuters, the head of the Securities and Futures Commission (SFC) will end its “opt-in” regulatory framework for crypto exchanges, bringing all trading platforms in Hong Kong under the control of the SFC – no matter if they trade securities or not.

The regulator is yet to explain if its move will see it impose stricter regulations on the Hong Kong crypto industry, which has been allowed to grow pretty much unchecked into one of the world’s largest crypto trading hubs.

In November last year, the SFC announced that exchanges can apply to be regulated by this Commission.

However, the crypto crackdown that effectively ended Mainland China’s dominance of the official crypto exchange market overnight in September 2017 will loom large in the minds of Hong Kong-based crypto enthusiasts.

An op-ed piece published by the state-run media outlet the People’s Daily has gained traction in the crypto community – and contains a number of references to how some Chinese citizens have been using crypto as a means of tax evasion. On a more positive note, though, the same article does also outline ways in which Chinese citizens can purchase crypto legally.

The article was co-authored by Shan Zhiguang, of the policy-making State Information Center think tank.

However, crypto users online believe that the move may be linked to a potentially more worrying trend in Mainland China, with reports about the arrest of Chinese-owned crypto exchange officials accelerating.

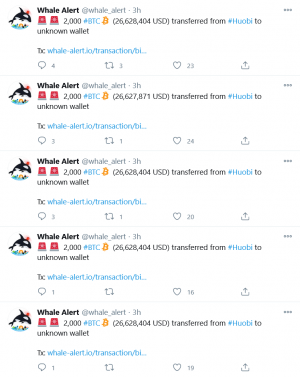

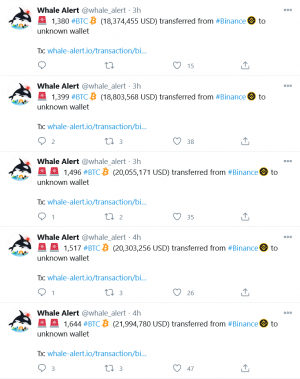

The Twitter-based blockchain tracker account Whale Alert has had a busy day with multiple reports of huge amounts of crypto moving off platforms such as Huobi and Binance in the past few hours.

___

Unconfirmed reports of the arrest of at least one senior Huobi official have been circulating online, and follow on from last month’s police investigation into Star Xu, the CEO of the OKEx exchange.

On Monday, responding to “inquiries and speculation from some users,” Huobi said that “We are currently operating normally, user assets are safe, and trading, deposits and withdrawals are operating as expected.”

In recent months, Huobi, Binance and OKEx have all made new moves in China where they claim their activities are purely blockchain technology-related.

On Twitter, some commentators have attempted to connect the dots between the Huobi reports and the SFC’s unexpected announcement.

Meanwhile, some claim the Hong Kong news is a sign Beijing is ready to “tighten the noose” on crypto.

Others opine that regulation was inevitable in Hong Kong, and could be on the cards elsewhere too.